Airbnb bonus depreciation rules 2026 matter because tax timing can change returns as much as occupancy and nightly rates. Sophisticated investors underwrite after-tax outcomes, especially when a short term rental includes meaningful furnishings, upgrades, or renovation scope.

From Nashville, where Airbnb investment properties remain active among disciplined operators, to other high-demand STR markets nationwide, experienced investors integrate tax strategy directly into acquisition underwriting.

Important: I am not a CPA. Always review eligibility and reporting with your CPA before acting.

Key Takeaways

- 100% bonus depreciation is restored for qualifying property acquired and placed in service after Jan 19, 2025.

- IRS Notice 2026-11 provides implementation guidance.

- Cost segregation can move components into 5, 7, or 15 year property eligible for accelerated expensing.

- STRs with average stays of 7 days or less, or 30 days or less with significant services, may avoid rental classification if material participation is met.

- Recapture at sale must be modeled in advance.

Airbnb Bonus Depreciation Rules 2026: What Changed?

Bonus depreciation was phasing down under prior law. The One Big Beautiful Bill restored 100% first-year expensing for qualifying assets placed in service after Jan 19, 2025.

This means many STR furnishings, appliances, and eligible interior improvements can be deducted immediately if they qualify in 2026.

What Bonus Depreciation Means for Airbnb Owners

Under IRC Section 168(k), qualifying assets with a recovery period of 20 years or less may be expensed faster, often in year one.

For STR owners, this commonly includes furniture, appliances, electronics, and certain interior improvements. Timing and placed-in-service documentation are critical.

Standard depreciation spreads deductions over years. Bonus depreciation accelerates them. The difference is cash flow timing.

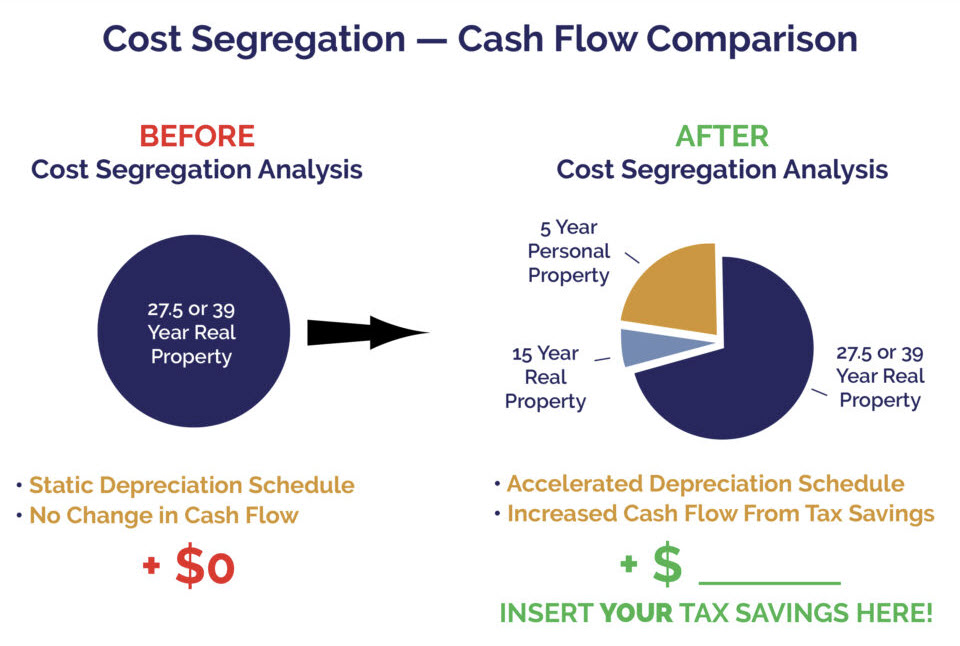

Why Cost Segregation Multiplies the Impact

Residential rental property is typically depreciated over 27.5 years. A cost segregation study identifies shorter-life components, often 5, 7, or 15 year property.

Those components may qualify for 100% bonus depreciation, which is where most first-year deduction power lives.

For STR investors furnishing at a high level, this modeling should happen before closing or renovation, not after. For example, a fully furnished Alora Nashville short term rental can generate substantial accelerated depreciation from interior components, sometimes exceeding $400,000 depending on furnishings.

The Short Term Rental Pathway to Offset Active Income

What many investors call the “short term rental loophole” is really about classification.

A short term rental may avoid being treated as a traditional rental activity under passive activity rules when:

- The average guest stay is 7 days or less, or

- The average stay is 30 days or less and significant services are provided

If one of these exceptions applies and you materially participate, losses may be treated as non-passive. Your CPA must confirm how this applies to your situation.

The 100 Hour Material Participation Rule

The “100 hour Airbnb rule” refers to one of the IRS material participation tests under Treasury Regulation §1.469-5T.

You may meet this test if:

- You work more than 100 hours during the year, and

- No other individual works more than you

If the short term rental also qualifies under the average stay exception and you meet this or another participation test, losses may be treated as non-passive.

Important: The 100 hour test alone does not guarantee qualification. Proper documentation and correct reporting are essential. Other tests exist, including a 500 hour test and additional aggregation pathways. The 100 hour test is simply the easiest possible route.

In practice, this requires real operational involvement such as guest communication, pricing strategy, booking oversight, and vendor coordination. This is not passive ownership.

Who Benefits Most From These Strategies

These strategies tend to be most impactful for investors with high marginal tax exposure, including:

- High income households, often $250,000+

- High W-2 earners with limited passive loss flexibility

- Business owners with significant active income

- Investors building tax-efficient wealth over time

Tennessee has no state income tax, which helps on the margin, but federal tax exposure is still the main driver of why deduction timing can matter.

Real Estate Professional Status

Real Estate Professional Status can expand how rental losses may be used against active income, but the requirements are strict and documentation heavy.

Common thresholds include more than 50% of personal services in real estate trades or businesses, at least 750 hours in real estate activities, and material participation in the rentals.

In many households, one spouse qualifies while the other maintains W-2 employment, creating a structured tax planning approach that should be guided by a CPA.

Eligible vs Non Eligible Improvements

Investors get tripped up here.

Many interior, non-structural components may qualify for shorter-life treatment. Structural and building-envelope work is often treated differently.

Roof, foundation, framing changes, major expansions, and many exterior improvements generally do not fall into the same accelerated buckets as interior components. Your CPA and a properly scoped cost segregation study help prevent misclassification.

Recapture and Exit Planning

Bonus depreciation accelerates deductions. It does not eliminate taxation.

If you sell, convert the property to personal use, or materially change its use, depreciation recapture can increase taxable income in the year of disposition. For most investors, the right question is not “is recapture bad,” but “what is my hold plan and exit plan.”

Common planning conversations with CPAs include longer hold periods and the potential role of a 1031 exchange where appropriate.

Practical 2026 Action Plan for STR Investors

- Confirm whether your property operations and average stay length support STR treatment under the applicable exceptions

- Separate structural vs eligible components

- Track placed-in-service dates and maintain documentation

- Log participation if you are pursuing non-passive treatment

- Run CPA modeling and consider Nashville mortgage rates and financing costs before acquisition

2026 Outlook for Airbnb Bonus Depreciation

Bonus depreciation 2026 remains at 100% under current law. Airbnb bonus depreciation rules 2026 allow full first-year expensing for qualifying property acquired and placed in service after Jan 19, 2025 under the One Big Beautiful Bill Act. Rather than phasing down as prior law scheduled, 100% bonus depreciation is restored on a permanent basis for eligible assets.

This creates a favorable planning environment for STR investors. The most durable strategy pairs the current bonus rules with disciplined underwriting, precise documentation, and a clear operational and exit plan that accounts for depreciation recapture.

Talk With a CPA First, Then Source the Right Property

I am not a CPA. My role is to help investors source and evaluate short term rental properties in Nashville and Middle Tennessee that tend to be strong candidates for cost segregation and bonus depreciation strategies, then coordinate with the CPA and cost segregation professionals who do the tax work.

If you want to pressure test a potential acquisition, upgrade plan, or furnishing scope against Airbnb bonus depreciation rules 2026, I can help you identify the right property profile and the right questions to bring to your CPA.

Frequently Asked Questions

Is bonus depreciation 100% in 2026 for STR owners?

For many qualifying assets, 100% bonus depreciation is available when qualified property is acquired and placed in service after Jan 19, 2025, subject to IRS rules and elections described in Notice 2026-11. Confirm your facts with your CPA.

What counts as placed in service?

Placed in service generally means installed and ready for its intended use. The timing and documentation of this step matters for claiming bonus depreciation.

Can a short term rental offset W-2 income?

In some cases, yes, when the STR meets an exception such as a 7-day average stay rule or a 30-day rule with significant services, and you materially participate. Your CPA should apply the passive activity rules to your specific facts.

Do I need a cost segregation study?

Not always. It is often most valuable when the property has meaningful component value, renovations, or high furnishing scope. A CPA can help determine whether the cost is justified.