The Middle Tennessee MLS (Realtracs) has reported April 2010 housing statistics. The following graphs and analysis are based on the greater Nashville residential single family homes and condos market only. Note: on April 30, the federal housing tax credit for first-time home buyers culminated giving rise to purchases that may have occurred later in the housing cycle.

The Middle Tennessee MLS (Realtracs) has reported April 2010 housing statistics. The following graphs and analysis are based on the greater Nashville residential single family homes and condos market only. Note: on April 30, the federal housing tax credit for first-time home buyers culminated giving rise to purchases that may have occurred later in the housing cycle.

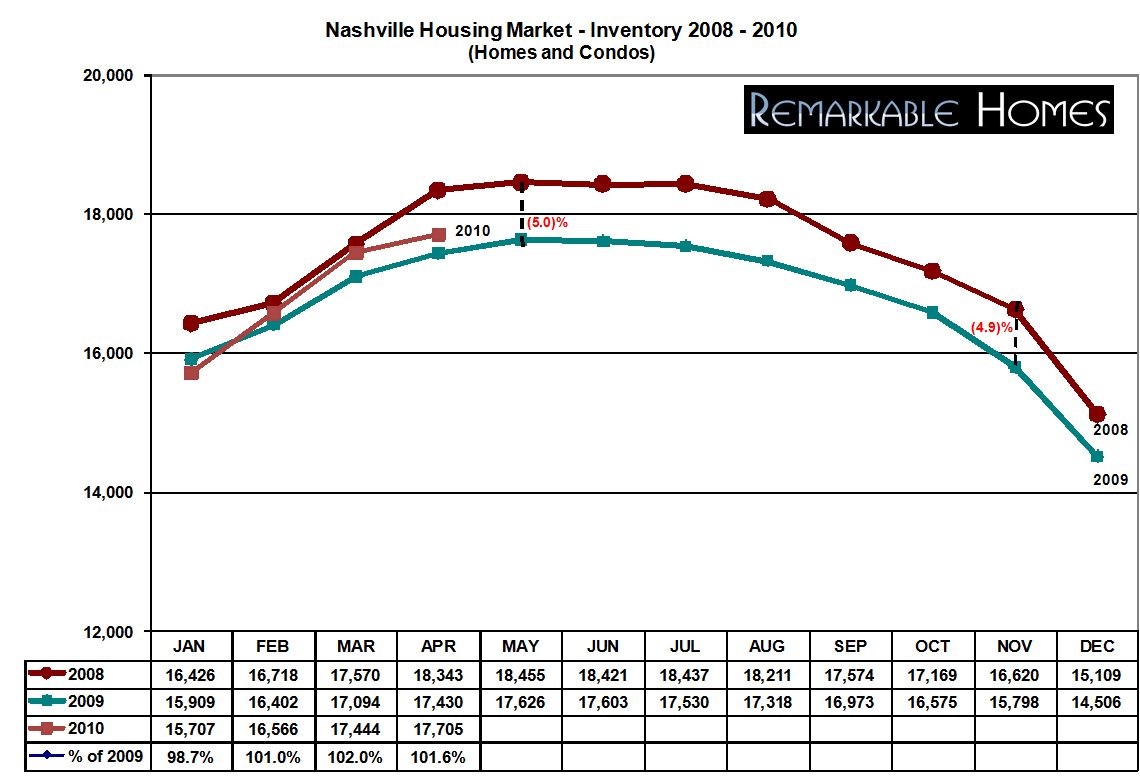

Total Inventory (Okay, Increasing)

Inventory levels continued to build in April, up 1.47 percent from March, up 11.28 percent since January 2010. There were a total of 17,705 active homes and condos listed in Nashville last month, compared to April 2009 when there were 17,430 on the market, a modest year over year increase of 1.55 percent. Interestingly, despite this year over year increase, the 2010 adjusted average monthly inventory is still lower than both 2009 and 2008 levels.

Pending Sales (Excellent, Inflated)

Pending sales in Nashville are up sharply in the first 4 months of 2010. Since January, pending sales have nearly doubled, soaring 193.43 percent higher. Additionally, total pending sales are 34.31% higher than their levels a year ago. In fact, the current 2,505 pending sales is the highest total in any month since June 2008 when there were 2,684 pending sales. This is not surprising news. The end of April coincided with the end of the federal $8,000 tax credit for first-time home buyers pushing a number of sales into April that would have normally occurred later in the summer. One must take some fraction of these sales and attribute them forward in an effort to annualize the data for a more accurate prediction of the coming months.

Closed Sales (Very Good, Inflated)

Just as with pending sales, the number of residential closings in Nashville has risen rather significantly. Since January, closings have more than doubled, increasing 208.52 percent. April’s total also represents a 16.9 percent increase over March. Compared to the same period in 2008, year over year closings have increased 35.49 percent when 1,516 properties closed. In addition, we have narrowed the gap over 2006 by another 6.11 percent during the past month. Again, let me caution you, these numbers have been inflated by the tax credit. Fascinatingly, April’s total closings are almost exactly the same as October 2009, the month prior to conclusion of the previous federal tax credit for first-time buyers. It is too early to compare the effect of each tax credit on Nashville sales, as the current tax credit concluded during a more advantageous time in our natural market cycle. Once an annualized analysis can be completed, I anticipate the ability to calculate the net effect of each tax credit.

Median Prices (Upward Trending, Stabilized)

April experienced the first month over month price increase since December 2009. Increasing 3.78 percent to $162,701, the median price in Nashville is now roughly equivalent to prices from a year ago. Compared to April 2009, the median price remained virtually identical, only falling 0.04 percent from $162,766. Furthermore, the current median price is only 0.0137 percent lower than the 12 month average median price for 2009. This evidence points towards a complete price stabilization in the Nashville market; however, it is still too early to tell whether the current tax credit has skewed the relative median price in a meaningful way or we have reached true stabilization.

Months of Inventory (Compressing)

Months of Inventory (Compressing)

Based on April’s closed sales, Nashville has 8.62 months of inventory currently on the market. Based on pending sales (contracts accepted but not closed yet) Nashville has only 7.07 months. The absorption rate has been significantly better over the past 3 months when there was 15.9 months of inventory based upon the same calculations – a 184.45 percent absorption rate increase. Do not let this rate increase fool you. Since 2003, the Nashville market has experienced a very similar 143.71 percent absorption increase over this same period annually.

Pragmatic Conclusions

As I begin to take seasonality into account, I am seeing that the first half of 2010 is shaping up to be quite similar to the second half of 2009. Yes, total closings and pending sales have risen sharply. Yes, the median price has increased, but the graph clearly indicates that the overall market levels are remarkably close to the same levels experienced towards the end of last year’s tax credit. The only appreciable difference is how quickly the 2010 numbers have risen. This dramatic rise is a simple combination of the Nashville housing market’s traditional seasonal gains plus some factor attributed to the conclusion of the current federal tax credit. Once adjusted, I anticipate being able to prove that the market has actually behaved in a slightly upward sloping linear manner. In other words, I should be able to mathematically prove that the Nashville real estate market has either begun to bottom out or has, in fact, bottomed out. Whether the market begins an appreciating cycle or is in for a double dip depends upon too many factors to list in this brief analysis.

Prediction

Many publications and periodicals will sensationalize the increasing volume of bank foreclosures and conclude that this increasing volume will have a negative effect on prices. This does not appear to be an accurate conclusion. Studies have shown that foreclosures have more than tripled in the Nashville market over the past 24 months and yet, the median price has still stabilized. So, what is the true difference between a bank selling at a stabilized lower price and a distressed homeowner doing the same? Not a whole lot from the market’s perspective.

{kind=link}