The Middle Tennessee MLS (Realtracs) has reported April 2010 housing statistics. The following graphs and analysis are based on the greater Nashville residential single family homes and condos market only. Note: on April 30, the federal housing tax credit for first-time home buyers culminated giving rise to purchases that may have occurred later in the housing cycle.

The Middle Tennessee MLS (Realtracs) has reported April 2010 housing statistics. The following graphs and analysis are based on the greater Nashville residential single family homes and condos market only. Note: on April 30, the federal housing tax credit for first-time home buyers culminated giving rise to purchases that may have occurred later in the housing cycle.

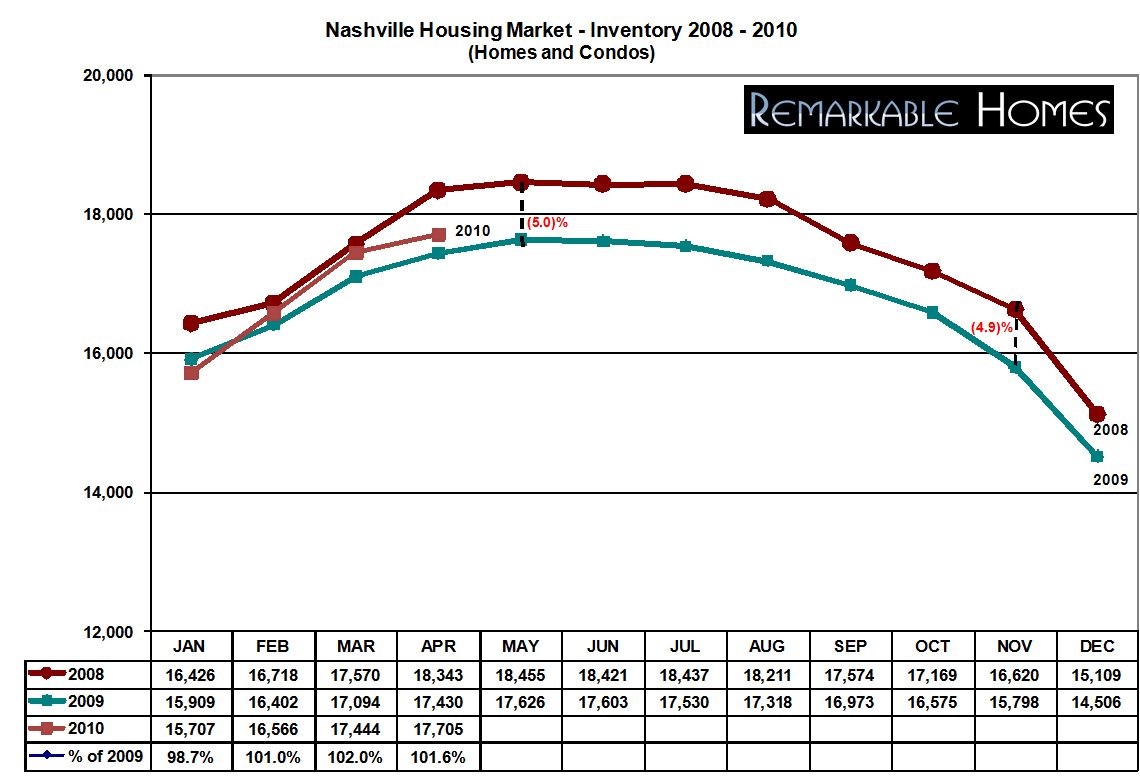

Total Inventory (Okay, Increasing)

Inventory levels continued to build in April, up 1.47 percent from March, up 11.28 percent since January 2010. There were a total of 17,705 active homes and condos listed in Nashville last month, compared to April 2009 when there were 17,430 on the market, a modest year over year increase of 1.55 percent. Interestingly, despite this year over year increase, the 2010 adjusted average monthly inventory is still lower than both 2009 and 2008 levels.

Pending Sales (Excellent, Inflated)

Pending sales in Nashville are up sharply in the first 4 months of 2010. Since January, pending sales have nearly doubled, soaring 193.43 percent higher. Additionally, total pending sales are 34.31% higher than their levels a year ago. In fact, the current 2,505 pending sales is the highest total in any month since June 2008 when there were 2,684 pending sales. This is not surprising news. The end of April coincided with the end of the federal $8,000 tax credit for first-time home buyers pushing a number of sales into April that would have normally occurred later in the summer. One must take some fraction of these sales and attribute them forward in an effort to annualize the data for a more accurate prediction of the coming months.

Closed Sales (Very Good, Inflated)

Just as with pending sales, the number of residential closings in Nashville has risen rather significantly. Since January, closings have more than doubled, increasing 208.52 percent. April’s total also represents a 16.9 percent increase over March. Compared to the same period in 2008, year over year closings have increased 35.49 percent when 1,516 properties closed. In addition, we have narrowed the gap over 2006 by another 6.11 percent during the past month. Again, let me caution you, these numbers have been inflated by the tax credit. Fascinatingly, April’s total closings are almost exactly the same as October 2009, the month prior to conclusion of the previous federal tax credit for first-time buyers. It is too early to compare the effect of each tax credit on Nashville sales, as the current tax credit concluded during a more advantageous time in our natural market cycle. Once an annualized analysis can be completed, I anticipate the ability to calculate the net effect of each tax credit.

Median Prices (Upward Trending, Stabilized)

April experienced the first month over month price increase since December 2009. Increasing 3.78 percent to $162,701, the median price in Nashville is now roughly equivalent to prices from a year ago. Compared to April 2009, the median price remained virtually identical, only falling 0.04 percent from $162,766. Furthermore, the current median price is only 0.0137 percent lower than the 12 month average median price for 2009. This evidence points towards a complete price stabilization in the Nashville market; however, it is still too early to tell whether the current tax credit has skewed the relative median price in a meaningful way or we have reached true stabilization.

Months of Inventory (Compressing)

Months of Inventory (Compressing)

Based on April’s closed sales, Nashville has 8.62 months of inventory currently on the market. Based on pending sales (contracts accepted but not closed yet) Nashville has only 7.07 months. The absorption rate has been significantly better over the past 3 months when there was 15.9 months of inventory based upon the same calculations – a 184.45 percent absorption rate increase. Do not let this rate increase fool you. Since 2003, the Nashville market has experienced a very similar 143.71 percent absorption increase over this same period annually.

Pragmatic Conclusions

As I begin to take seasonality into account, I am seeing that the first half of 2010 is shaping up to be quite similar to the second half of 2009. Yes, total closings and pending sales have risen sharply. Yes, the median price has increased, but the graph clearly indicates that the overall market levels are remarkably close to the same levels experienced towards the end of last year’s tax credit. The only appreciable difference is how quickly the 2010 numbers have risen. This dramatic rise is a simple combination of the Nashville housing market’s traditional seasonal gains plus some factor attributed to the conclusion of the current federal tax credit. Once adjusted, I anticipate being able to prove that the market has actually behaved in a slightly upward sloping linear manner. In other words, I should be able to mathematically prove that the Nashville real estate market has either begun to bottom out or has, in fact, bottomed out. Whether the market begins an appreciating cycle or is in for a double dip depends upon too many factors to list in this brief analysis.

Prediction

Many publications and periodicals will sensationalize the increasing volume of bank foreclosures and conclude that this increasing volume will have a negative effect on prices. This does not appear to be an accurate conclusion. Studies have shown that foreclosures have more than tripled in the Nashville market over the past 24 months and yet, the median price has still stabilized. So, what is the true difference between a bank selling at a stabilized lower price and a distressed homeowner doing the same? Not a whole lot from the market’s perspective.

{kind=link}

May 20, 2010, 12:00 pm

Fantastic market analysis. I appreciate that you boil these numbers down to their practical implications and make it available to everyone. But as a rule, reducing the numbers to this level only tells us more simply what has happened, not what will happen. Your analysis has helped me form my view on the market, and I look forward to a follow up down the road.

May 20, 2010, 2:05 pm

Thank you Buck. I am actually going to be posting a predictive weighted average mean price compared with volume of sales study today and it does appear that home prices in the Nashville market won't completely recover until May of 2011. However, if you try to time the bottom, you'll almost always miss it. I am recommending buying this Fall.

May 20, 2010, 3:20 pm

May 28, 2010, 7:09 pm

July 13, 2010, 7:41 pm

Just curious if you've noticed any significant change in new condo prices since the tax credit expired on 4/30/10. Since buyers had until 6/30/10 to close, it seems inevitable prices will fall, but that may not yet be reflected in prices just yet. (Also, I thought I heard the time to close had been extended beyond 6/30/10 for contracts prior to 4/30/10, which may further delay the impact of the loss of the tax credit.)

July 21, 2010, 11:26 pm

The condo market has softened on the whole since the end of the tax credit, but the good buildings are still booking sales at higher than expected rates and prices. Since 4/30/2010:

The Adelicia has closed 7 condos and has 1 pending. The average price/ft is $358.27/ft. Wow. The Icon has closed 30 condos and has 13 pending. The average price/ft is $302.96/ft. Very respectable

Certainly, I don’t want to paint a rosier picture than reality in the downtown condo market. The Viridian, Encore, and Terrazzo sales and slowed significantly and I don’t even show a MLS recorded closing for The West End during this period.

July 27, 2010, 1:41 pm

Below is a front page NBJ article from Friday on condo sales, pricing and foreclosures. Buyers in Icon and Encore are now starting to cut their losses and sell for $50k or more less than they paid for their units. The Icon developer disputed that this is having an impact but here is a quote from a broker that is handling a short sale in the Icon:

As the agent for a short-sale in Icon in the Gulch, Storolis said any price reduction on the unit has been met in kind on new units by the developers, a partnership between Bristol Development Group and MarketStreet Enterprises. “The developers are watching us do this stuff, and they respond to us,” Storolis said

Read more: Downtown condos battle falling prices, resale values – Nashville Business Journal

http://nashville.bizjournals.com/nashville/stor…

July 29, 2010, 10:45 pm

Falcon2 – I realize that I am about to start a philosophical debate with one of the most knowledgeable people in the Southeast, but here goes nuth’in:

Of the 513 condo owners within these 15 buildings, I only show less than 12% of these owner units for sale on the MLS. The vast majority are in the Viridian. I understand the point that 27% of all condo owners could potentially be underwater if they were to sell, but that number is not relevant to how many are selling or are going to be selling in this market. I also realize that many condo owners would place their condos on the market if they could sell for more than what they paid, but isn’t that statement true for most any commodity?

I am certainly not disagreeing with the fact that if one had to sell their condo right now, in this market, they have a better than average chance of selling for less than what they paid in 2005-2008. I also agree that a certain percentage of the current 513 condo owners will run this unfortunate gauntlet over the next few years. But, I do not believe that 27% of the 513 condo owners will lose money when they do chose to sell their condos.

I am also not worried about any current negative or positive equity in any real estate asset at the moment. For the most part, banks have frozen everyone’s home equity lines no matter how much positive equity you may have. It’s a non-starter for me at the moment, at least, until banks free up credit lines in the future.

Comparatively speaking, I also agree that the downtown condo market has fared worse than the average residential property in Tennessee. However, this is to be expected as the core sample size is drastically different. The ability for a much larger sample size to normalize or avoid the extremes is a well documented economic principal. In turn, I would expect when properties begin to appreciate, the downtown condo market will appreciate faster than the average Tennessee property.

Newspapers, TV newscasts and the general public seem to enjoy pointing their fingers towards downtown, but the people who live downtown tell a much different story. The development of downtown Nashville as a residential haven is not over the hump, but give us another decade and all of the growing pains will be met with reward.