Market Summary

- Nashville 30-year fixed mortgage rate averaged 6.00% during March 2 to March 6, 2026.

- Nashville 15-year fixed mortgage rate averaged 5.43% across Middle Tennessee.

- FHA 30-year mortgage rates held near 6.01% for qualified borrowers.

- The 10-year Treasury yield remained near 4.14% during the week.

- Mortgage spreads remained near 1.86%, consistent with long-term averages.

- Federal Reserve policy remained restrictive, with no major balance sheet changes in the latest H.4.1 report.

Mortgage Rate Dashboard

This Week’s Rates

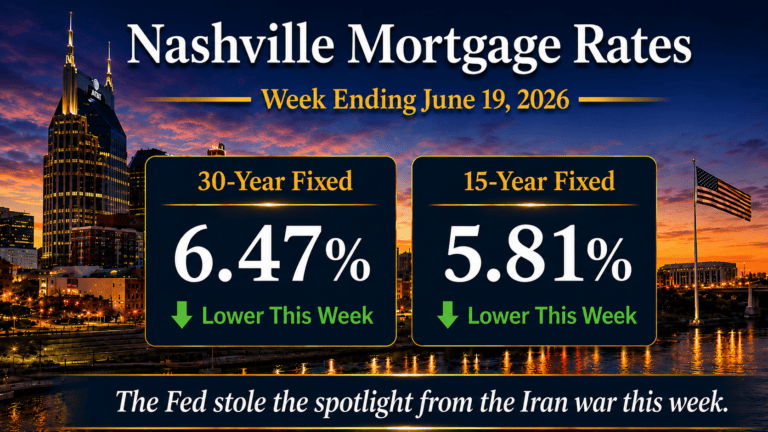

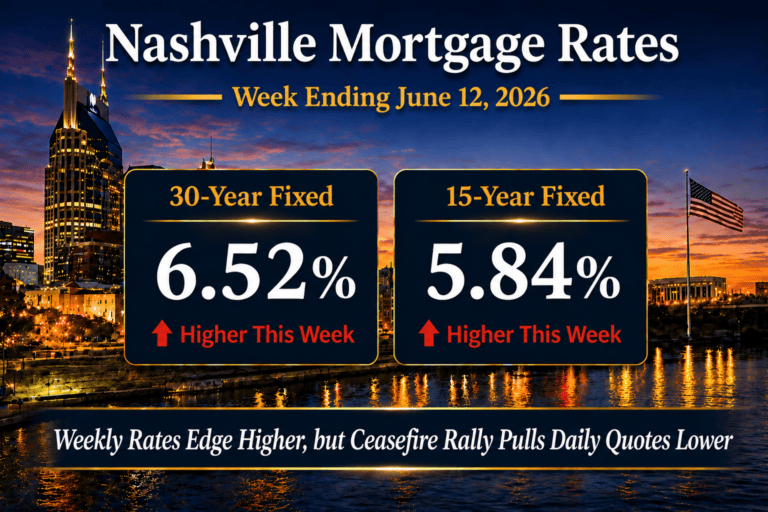

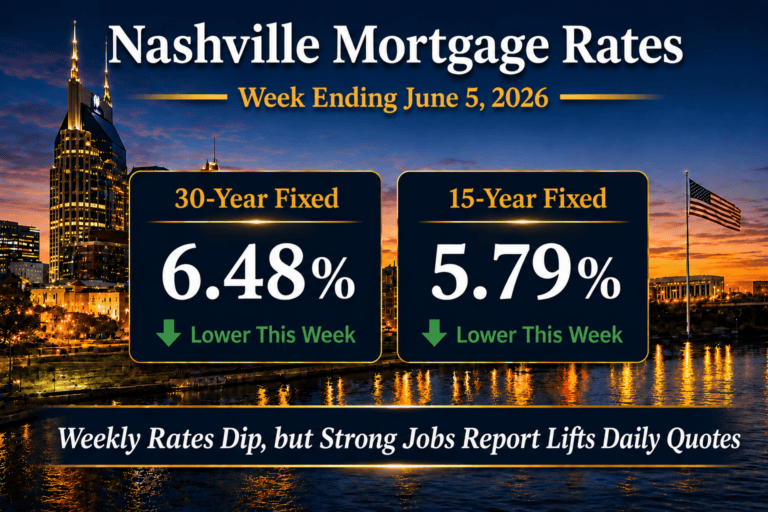

Freddie Mac reported that the average 30-year fixed mortgage rate rose slightly to 6.00% from 5.98% the previous week, while the 15-year fixed rate moved to 5.43%.

Although the move higher was small, it marked a shift from the extremely calm environment seen the previous week. The week ending February 27 produced one of the lowest volatility periods in mortgage rates seen in years, with rates holding within an unusually tight range near 6%.

This week, however, reminded markets that the forces influencing mortgage rates remain complex and often global in nature.

What Is Driving Mortgage Rates Right Now?

This has been an interesting week for mortgage markets.

Coming into the week, the bond market appeared to be gaining momentum toward lower interest rates. Mortgage-backed securities and the 10-year Treasury were showing signs that a rally could continue after mortgage rates reached multi-year lows in late February.

Then the weekend developments involving Iran introduced a new layer of uncertainty into global markets.

When geopolitical tensions increase, two competing forces often influence interest rates.

The first is what economists call a flight to safety. During periods of global uncertainty, investors frequently move money into safer assets such as U.S. Treasury bonds and mortgage-backed securities. When demand for those assets increases, yields tend to fall, which generally supports lower mortgage rates.

The second force involves inflation risk, particularly through energy prices. Oil is a key input for transportation and shipping costs across the global economy. Historically, every $10 increase in oil prices can add roughly 0.2% to inflation expectations. Higher inflation expectations typically push interest rates higher.

Another factor is government financing. When geopolitical tensions increase, governments sometimes expand spending. Because the United States operates with a budget deficit, additional spending is often financed through issuing more Treasury bonds. Increased Treasury supply can push yields higher, which would put upward pressure on mortgage rates.

The key question for markets right now is which of these forces ultimately dominates.

History provides some perspective. Since 2020 there have been several major geopolitical events involving the Middle East. In each case, both oil prices and Treasury yields initially moved higher, but within roughly 10 to 15 days markets generally stabilized and often returned to previous levels.

One reason reactions may be more muted today is that the United States is significantly more energy independent than it was several decades ago. Global energy shocks still matter, but their impact on the domestic economy is often less severe than in the past.

Toward the end of this week, economic data began shifting attention away from geopolitics and back toward the domestic economy.

Retail sales came in slightly better than expected, while the Nonfarm Payrolls report showed a surprising decline of roughly 92,000 jobs compared with expectations for growth. The unemployment rate also ticked slightly higher to 4.4% from 4.3%.

That softer labor market data helped the 10-year Treasury rally modestly, which in turn helped stabilize mortgage rates after earlier volatility in the week.

The overall takeaway is that geopolitical events temporarily interrupted the downward momentum in mortgage rates, but the long-term trend continues to be influenced primarily by economic data. For ongoing context and historical comparisons, visit Nashville Mortgage Rates Today.

Macro Snapshot | March 6, 2026

The 10-Year Treasury and Mortgage Spreads

Mortgage rates tend to track the 10-year Treasury yield closely, though the relationship is not exact.

Historically, the spread between mortgage rates and the 10-year Treasury averages between 1.7% and 2.0%.

With the 10-year Treasury near 4.14% and mortgage rates around 6.00%, the current spread of roughly 1.86% remains within normal historical ranges.

This normalization is important. During periods of market stress in 2022 and 2023, mortgage spreads widened significantly due to Federal Reserve tightening and reduced demand for mortgage-backed securities. As spreads return toward historical norms, mortgage rates can decline even if Treasury yields remain stable.

Strategic Borrower Considerations in Today’s Market

Rate Volatility

Last week produced record low volatility for mortgage rates. This week was more active, largely due to rising oil prices and geopolitical uncertainty. However, in the broader context rates remain within a narrow range around 6%.

Lower volatility tends to benefit borrowers because lenders can price loans more confidently without building large risk premiums into mortgage rates.

Adjustable vs Fixed Mortgage Decisions

Adjustable-rate mortgages continue to represent a modest portion of new loans. With fixed mortgage rates hovering near multi-year lows, many borrowers prefer the predictability of locking a fixed rate near 6% rather than taking on future rate uncertainty.

Treasury Auctions and Market Signals

Bond markets will continue to watch economic data closely. Upcoming inflation reports, Treasury auctions, and employment data will likely determine whether rates remain stable or begin another move lower.

What This Means for Nashville and Middle Tennessee

For buyers across Nashville, Brentwood, Franklin, and surrounding communities, mortgage rates hovering near 6% provide a much more stable environment than the volatility experienced earlier in the rate cycle.

Lower borrowing costs combined with improving rate stability may gradually encourage more buyers and sellers to re-enter the housing market as the spring season approaches.

While affordability remains a challenge due to home prices, the recent improvement in mortgage rates is helping rebuild confidence in the market.

What to Watch Next Week

Several key developments could influence mortgage rates next week:

- Treasury yield movements following economic data releases

- Inflation data and commodity price trends

- Mortgage application activity reported by the MBA

- Federal Reserve commentary ahead of upcoming policy meetings

If Treasury yields move lower again, mortgage rates could revisit the sub-6% range seen in late February.