Outlook for 2026

Market Data, Development Trends, and Investor Insights for the Nashville Short-Term Rental Market

Grant Hammond

Nashville STR Market Specialist

Published March 2026

More than 550 Nashville short-term rental transactions represented

Table of Contents

- Executive Summary

- Nashville STR Market at a Glance

- How This Report Was Built

- Why Nashville Became a National Airbnb Destination

- The Evolution of Nashville’s STR Development Model

- Nashville STR Development Timeline

- The Nashville Airbnb Market Cycle, 2020 to 2025

- Geographic Concentration of STR Investment

- Nashville STR Development Heat Map and Cluster Analysis

- Major Nashville Airbnb Investment Neighborhoods

- The Two Nashville STR Markets

- Revenue Benchmarks and Property Performance

- Typical Nashville Airbnb Operating Costs

- Nashville STR Financing Environment

- Nashville STR Tax Advantages for Investors

- Nashville STR Zoning, Regulation, and Permitting

- Pricing Stability, Developer Incentives, and Effective Pricing

- The Nashville STR Supply Pipeline

- How Nashville Compares to Other Inland STR Markets

- Why Nashville Attracts Out-of-State Investors

- The Nashville STR Investment Environment in 2026

- What Makes a Successful Nashville Airbnb Investment

- What Investors Should Watch Next

- Data Sources, Methodology, and Limitations

- Author Participation Disclosure

- About the Author

1. Executive Summary

Nashville’s short-term rental market has moved through three distinct phases during the past five years: rapid investor expansion, development-driven price growth, and a more selective and increasingly buyer-friendly investment environment.

In the early 2020s, historically low interest rates, accelerating tourism growth, and national investor attention helped transform Nashville into one of the most active Airbnb investment markets in the United States. By 2025, that initial surge had matured into a more disciplined market environment where investment success increasingly depends on property type, location, zoning viability, revenue durability, and the ability to negotiate favorable acquisition terms.

This report analyzes nearly 1,300 publicly recorded Nashville short-term rental transactions between 2020 and 2025, alongside development-level observations and brokerage insight informed by more than 550 Nashville STR transactions represented by Grant Hammond. The combination of transaction-level data and real market participation allows this report to move beyond general commentary and provide a practical framework for understanding how the Nashville STR market operates today.

Several conclusions emerge from the data.

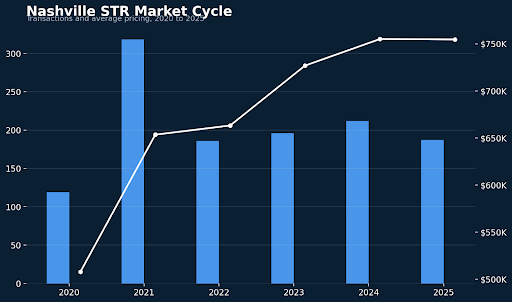

First, the Nashville STR market expanded rapidly between 2020 and 2021, culminating in 358 recorded STR closings in 2021, the peak year of investor expansion.

Second, while transaction volume moderated after 2021, pricing remained resilient. This occurred in part because the market increasingly shifted toward larger and more expensive purpose-built STR communities, replacing smaller scattered units that characterized earlier phases of the market.

Third, investor activity became concentrated in several redevelopment corridors surrounding downtown Nashville, particularly 37207, 37203, and 37209, where tourism access, redevelopment opportunity, and zoning eligibility aligned.

Fourth, the strongest-performing property type increasingly became the 4 bedroom, 4 bathroom STR townhome with rooftop deck, reflecting Nashville’s group-oriented tourism economy and the demand for accommodations capable of hosting larger visitor groups.

Fifth, by 2025 and into 2026, many developers began preserving list prices while offering meaningful buyer incentives such as closing cost credits, furnishing allowances, and rate buydowns. As a result, effective acquisition costs in several new developments are often lower than headline pricing suggests.

The broader takeaway is constructive.

Nashville continues to benefit from long-term structural demand driven by tourism, entertainment, and event-based visitation. The speculative “anything will sell” phase of the early expansion cycle has passed. In its place is a more mature investment environment where information, product selection, and disciplined underwriting play a much larger role.

For experienced investors, this shift may represent opportunity rather than risk. A more rational market environment often allows buyers to secure stronger long-term positions than were available during the height of the expansion cycle.

Figure 1. Key findings from the Nashville Airbnb Market Report. Source: Grant Hammond Nashville STR Market Analysis.

2. Nashville STR Market at a Glance

The Nashville Airbnb market is best understood through a handful of headline indicators that summarize the scale, maturity, and direction of the sector.

- Transactions analyzed: 1,200+ publicly recorded STR sales

- Transactions represented by Grant Hammond: 550+

- Peak expansion year: 2021

- Peak annual STR closings: 358

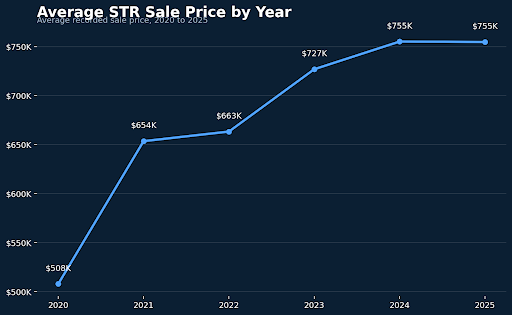

- Average STR sale price in 2025: approximately $754,000

- Annual Nashville visitors: approximately 17 million in 2025

- Primary STR investment corridors: 37207, 37203, 37209

- Dominant STR property type: 4 bedroom, 4 bathroom townhomes with rooftop decks

- Largest development distribution highlighted in this report: Muse Nashville, with 55 total units and 54 sales represented by Grant Hammond during initial sellout

These metrics tell a coherent story. Nashville is not a fringe Airbnb market. It is a market with real scale, defined corridors of investment, specialized property types, and a growing body of historical transaction data. It is also a market where local experience matters. Investors who understand Nashville’s zoning realities, tourism geography, and development patterns have a meaningful advantage over those evaluating the city from a distance.

3. How This Report Was Built

This report was built to answer a simple investor question: How does the Nashville Airbnb market actually work today?

To answer that question, this analysis combines 4 sources of information.

The first is publicly recorded transaction data for Nashville STR property sales between January 2020 and December 2025. This dataset provides visibility into acquisition activity, pricing, geographic concentration, and market evolution.

The second is development-level market knowledge drawn from direct participation in numerous STR projects across the city. Several developments discussed in this report were originally marketed and sold with Grant Hammond representation during their initial sales phases.

The third is operational market intelligence informed by how actual investors evaluate Airbnb opportunities in Nashville. That includes practical understanding of revenue benchmarks, operating costs, financing structures, zoning constraints, permit requirements, and buyer behavior.

The fourth is public policy and market context, including official information from Metro Nashville’s Codes Department, Nashville tourism sources, and current IRS guidance relevant to STR investors. Metro Nashville’s permitting and zoning framework also informs the regulatory analysis in this report.

No single dataset captures every STR property operating in Nashville. Some properties were built and retained by developers, some were converted to Airbnb use without a sale, and some transactions occurred in ways that are not fully reflected in public MLS records. For that reason, this report should be read as a detailed study of publicly sold STR investment properties and the market structure around them, not as a complete census of every Airbnb in Davidson County.

Market Interpretation

Because this report is grounded in actual transactions rather than generic commentary, it offers a practical view of how Nashville’s short-term rental market has developed, how it is functioning today, and where more informed investors may still hold an advantage.

4. Why Nashville Became a National Airbnb Destination

Nashville’s rise as one of the most prominent Airbnb investment markets in the United States did not occur by accident. It emerged from several overlapping structural forces that transformed the city into one of the fastest growing tourism economies in the country.

Understanding these forces helps explain why Nashville became a national short term rental market rather than simply a regional tourism destination.

Tourism Growth

The most visible driver is Nashville’s sustained tourism expansion.

According to Visit Music City, Nashville welcomed approximately 17 million visitors in 2025, continuing a multi-year pattern of strong visitor growth and rising tourism spending. The city’s tourism economy has expanded significantly over the past decade, supported by new entertainment venues, convention activity, major events, and national media visibility.

This growth matters because the Nashville STR market is fundamentally a tourism-driven real estate market. Without sustained visitor demand, the development of purpose-built STR communities would never have reached the scale now visible across the city.

A Tourism Economy Built Around Group Travel

The structure of Nashville’s tourism demand also plays a critical role.

Nashville is not simply a city people visit. It is a city people visit together.

Bachelor and bachelorette parties, concert weekends, sporting events, conventions, festivals, and music tourism all generate strong group travel patterns. Visitors frequently arrive in groups that prefer to stay together rather than in separate hotel rooms.

That demand profile strongly favors larger Airbnb properties, which helps explain why four-bedroom STR townhomes with rooftop entertainment space have become one of the dominant property types in the Nashville investment market.

Concentrated Entertainment Geography

Another major advantage for the Nashville STR market is the unusually concentrated geography of its tourism activity.

Many cities have tourism, but Nashville’s entertainment district is highly centralized around Lower Broadway, the downtown core, and Music City Center. Professional sports venues and major event spaces sit within close proximity to this entertainment district.

Because visitor activity is geographically concentrated, investors can more easily identify which locations are likely to perform well. Properties within a short rideshare distance of downtown entertainment tend to outperform more distant locations because they align with how visitors actually experience the city.

Urban Redevelopment and Investment Capital

Nashville’s tourism expansion occurred at the same time the city was experiencing rapid urban redevelopment.

Population growth, corporate relocations, and sustained construction activity created redevelopment corridors surrounding downtown Nashville. These areas provided opportunities for developers to build townhome-style communities designed specifically for short-term rental use.

Without these redevelopment opportunities, the Nashville STR market would likely have remained limited to smaller scattered properties rather than evolving into purpose-built investment communities.

Regulatory Structure

The final driver is Nashville’s regulatory framework.

While the city’s short-term rental regulations are more structured than many observers assume, they have historically allowed non-owner-occupied STR activity in specific zoning contexts. These rules created viable pathways for investor participation while also concentrating development into a limited number of neighborhoods.

Over time, this regulatory structure helped shape the geographic identity of the Nashville STR market by directing development toward corridors where zoning, redevelopment opportunity, and tourism access aligned.

Market Interpretation

Taken together, these factors created a rare combination of conditions.

Nashville offers strong tourism demand, a highly concentrated entertainment district, development corridors capable of supporting new construction, and regulatory pathways that historically allowed investor participation. Few inland U.S. cities possess all of these characteristics simultaneously.

That combination explains why Nashville evolved into one of the most visible short-term rental investment markets in the country and why it continues to attract national investor attention today.

5. The Evolution of Nashville’s STR Development Model

The Nashville STR market did not develop all at once. Instead, it evolved through several stages, each of which changed the type of properties investors considered attractive Airbnb acquisitions.

Understanding this progression helps explain why today’s Nashville STR market is dominated by purpose-built communities rather than scattered individual properties.

Phase 1: Condo-Based STR Investing

In the earliest phase of the modern Nashville Airbnb market, many investors focused on smaller condominium units located close to downtown. These properties were attractive because they offered immediate proximity to the entertainment district and were relatively easy for investors to understand. In many ways, they functioned as alternatives to hotel rooms in a rapidly growing tourism market.

However, these units also had structural limitations. Studio and 1 bedroom condominiums are inherently limited in guest capacity. Their success depends heavily on walkability, strong occupancy rates, and nightly pricing that can remain competitive with nearby hotels.

As hotel construction accelerated in downtown Nashville, these smaller STR units increasingly faced competition from properties offering larger amenity packages and more standardized hospitality operations.

Phase 2: Early STR Projects

The next phase of the market emerged when developers began designing projects specifically intended for short-term rental use rather than adapting traditional residential product. Early examples included Lyric at Cleveland Park*, Monty*, and Scovel Row*. These communities introduced features that would later become common in the Nashville market, including larger guest counts, rooftop gathering space, and layouts better suited to group stays.

This stage marked an important turning point. The Nashville STR market was no longer simply a resale market for existing properties. It was becoming a development-driven market.

Phase 3: Purpose-Built STR Communities

By the early 2020s, the market had decisively shifted toward purpose-built STR communities. Developers were no longer experimenting with the concept. They were refining it.

Projects such as Raven*, Skyline*, Starlet Townhomes*, Horizon River District*, Alora Nashville*, Vistas at Katie Hill*, and Musica Music Row* illustrate this phase of development. These communities were designed from the outset around group-oriented travel demand and typically featured consistent floor plans, larger guest capacity, rooftop entertainment areas, and layouts designed for short-term rental operations.

During this phase, the defining product type in the Nashville STR market became the 4 bedroom, 4 bathroom townhome with rooftop deck, which aligned closely with the city’s tourism profile and revenue dynamics.

Market Interpretation

The evolution of Nashville’s STR development model helps explain why the market today looks very different from the early Airbnb landscape. Rather than consisting of scattered individual units, the Nashville STR sector has increasingly become a specialized development category designed specifically to serve group-oriented tourism.

Investors who continue to evaluate Nashville primarily through the lens of the early condo-based STR market may overlook where the strongest opportunities have emerged. The modern Nashville STR market is largely defined by purpose built communities designed around the way visitors actually experience the city.

*Developments marked with an asterisk were originally marketed and sold with Grant Hammond representation during the initial sales phase.

6. Nashville STR Development Timeline

Examining the market chronologically helps illustrate how quickly Nashville’s short-term rental ecosystem developed and matured.

2019 to 2020:

The first recognizable wave of purpose-built STR developments begins to appear in redevelopment corridors surrounding downtown Nashville. During this period, developers began testing townhome-style communities designed to host larger groups rather than relying primarily on downtown condominium units.

These early projects helped demonstrate that Nashville’s tourism economy could support properties designed specifically for group-oriented short-term rental use.

2021 to 2022:

This period marked the most rapid expansion of investor activity in the Nashville STR market. Transaction volume accelerated sharply as historically low interest rates, strong tourism demand, and rising national awareness of Nashville attracted a growing number of investors.

One of the most visible examples of this expansion phase was Muse Nashville*, a 55-unit purpose-built downtown STR condominium development where Grant Hammond represented 54 of the 55 sales, including 40 closings in 2021 and 14 in 2022. The rapid sellout of Muse became a clear illustration of the strong investor appetite that characterized the peak expansion phase of the market.

2023 to 2025:

Following the expansion period, the market began to mature. Additional STR developments were delivered across multiple redevelopment corridors, and developers continued refining product design.

During this phase, the market’s center of gravity increasingly shifted toward larger townhome-style properties designed for group travel. Transaction activity stabilized compared with the peak expansion years, but pricing remained firm as the typical STR product became larger, newer, and more specialized.

Market Interpretation

Viewed as a whole, the timeline shows a market that moved from experimentation to expansion and then to specialization in a relatively short period.

Investors who understand where the Nashville STR market sits within this progression are better positioned to interpret both current opportunities and potential risks. Markets rarely move in straight lines, but understanding the development cycle provides important context for evaluating how the sector may evolve going forward.

7. The Nashville Airbnb Market Cycle, 2020 to 2025

The Nashville STR market cycle over the past several years can be understood in 3 phases: expansion, price growth, and normalization. Each phase reflects changes in investor behavior, development activity, and the broader economic environment.

Expansion Phase

The expansion phase occurred between 2020 and 2021. During this period, historically low interest rates and surging investor demand drove a sharp increase in acquisition activity across Nashville’s short-term rental market.

Investor enthusiasm accelerated rapidly as the city’s tourism profile continued to grow and purpose-built STR communities began attracting national attention.

Key Takeaway

Nashville’s STR market expanded rapidly between 2020 and 2021 before transitioning toward a more selective investment environment in the years that followed.

By 2021, the market recorded 358 STR closings, representing the high-water mark for investor expansion within the dataset used in this report.

Price Growth and Development Expansion

The second phase of the cycle occurred as developers began delivering larger and more specialized STR product. Even though transaction counts moderated after the peak expansion period, average sale prices continued to rise.

This dynamic reflected a structural shift in the type of properties being built and sold. Rather than smaller scattered units, the market increasingly consisted of purpose-built STR communities, many of which featured larger townhome-style properties designed for group travel.

Because these properties were both larger and more specialized, the average transaction price increased even as the pace of acquisitions slowed.

Key Takeaway

Average STR sale prices continued rising through 2024 despite lower transaction velocity, reflecting both product evolution and the scarcity of viable STR development locations..

Normalization Phase

By 2025, the Nashville STR market had moved beyond its early expansion stage. The market environment became more selective, and investors began placing greater emphasis on location quality, property design, revenue durability, and effective pricing.

Developers continued delivering projects during this period, but transactions increasingly relied on buyer incentives and negotiated terms rather than the rapid sell-through environment that characterized the expansion phase.

Market Interpretation

This distinction is important. The current market should not be interpreted as weak. It is better understood as a more disciplined investment environment.

In early-stage markets, strong momentum can make many properties appear attractive. In more mature markets, performance differences become clearer. The strongest properties continue to perform well, while weaker assets become easier to identify.

The Nashville STR market appears to have entered this more mature phase, where property fundamentals and investor discipline play a larger role in acquisition decisions.

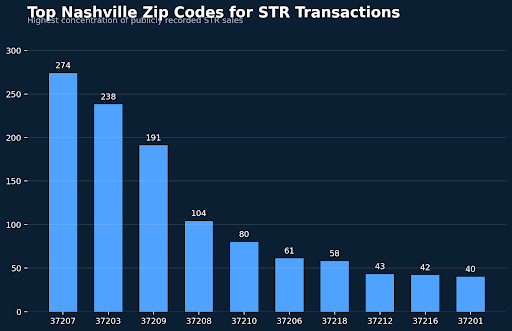

8. Geographic Concentration of STR Investment

One of the clearest patterns in the data is that Nashville’s short-term rental investment activity is geographically concentrated rather than evenly distributed across the metropolitan area.

A large share of investor acquisitions has occurred in just 3 zip codes surrounding the downtown core:

37207, 37203, and 37209.

These areas form a redevelopment ring around downtown Nashville where tourism proximity, development opportunity, and zoning eligibility intersect.

Key Takeaway

Investor activity is heavily concentrated in a small number of redevelopment corridors located within a short distance of downtown Nashville.

Why These Corridors Emerged

Tourism Access

The first factor is proximity to Nashville’s tourism economy. These corridors sit within a short rideshare distance of Lower Broadway and the downtown entertainment district, where a large share of visitor activity occurs.

Redevelopment Opportunities

The second factor is redevelopment potential. Over the past decade, these neighborhoods offered zoning-eligible infill sites and redevelopment parcels that could support townhome-style construction and purpose-built STR communities.

Zoning Constraints

The third factor is Nashville’s regulatory framework. Metro Nashville has increasingly restricted where non-owner-occupied STR properties can legally operate. As a result, development activity naturally concentrated in areas where zoning allowed investor-owned short-term rentals.

Market Interpretation

The Nashville STR market is not evenly distributed across the city. It is corridor-driven.

Investors who understand these geographic corridors gain a clearer framework for evaluating property performance, regulatory viability, and the likely direction of future development activity.

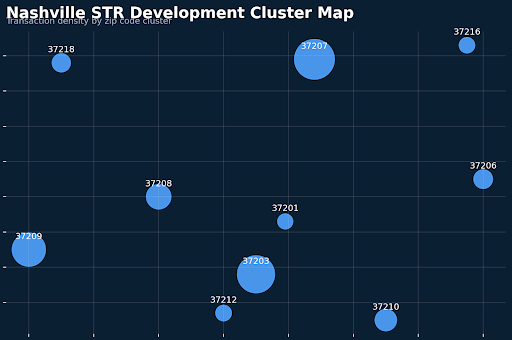

9. Nashville STR Development Heat Map and Cluster Analysis

The visual cluster pattern in the dataset reinforces what the zip code analysis already suggests: Nashville’s STR market is highly concentrated rather than evenly distributed across the city.

The heat map illustrates where the greatest density of STR development and investor acquisitions have occurred during the past several years. These clusters tend to appear in neighborhoods that combine redevelopment opportunity with practical rideshare access to the downtown entertainment district.

The cluster map provides an additional perspective by showing how sharply STR activity declines outside of the most active corridors. While short-term rentals exist throughout the metropolitan area, the majority of investor-oriented development has occurred within a relatively narrow ring surrounding downtown Nashville.

Key Takeaway

The strongest STR development clusters occur in a limited number of neighborhoods where tourism proximity, zoning eligibility, and redevelopment potential align.

Market Interpretation

Geographic concentration plays a critical role in the Nashville STR market. It influences not only competition among properties but also resale liquidity, permit viability, and future development strategy.

In Nashville, location matters in two ways. It matters because visitors want convenient access to the downtown entertainment district. And it matters because local zoning regulations limit where investor-owned STR properties can legally operate.

The result is a market where development naturally clusters in a small number of viable corridors rather than dispersing evenly across the city.

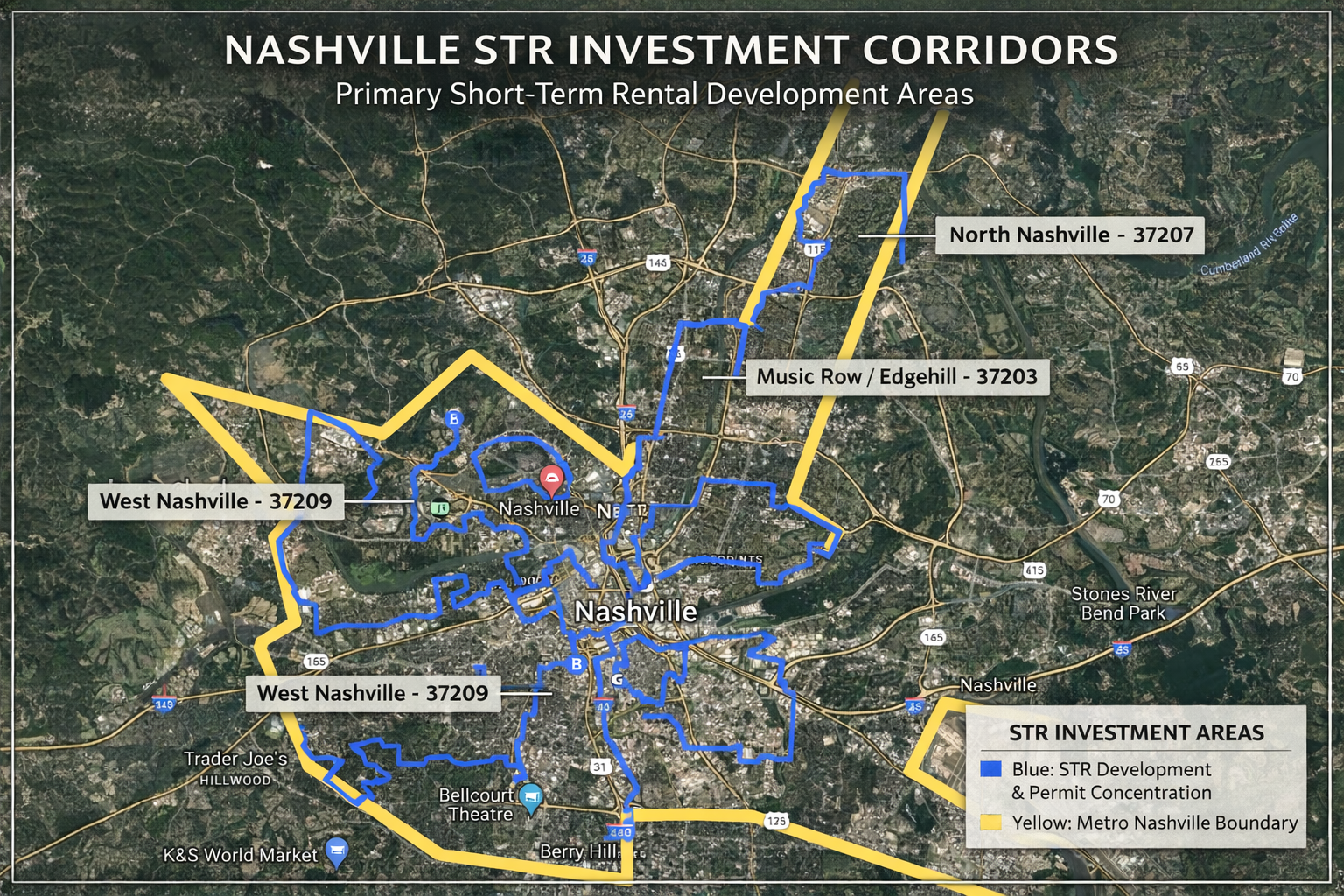

10. Major Nashville Airbnb Investment Neighborhoods

Short-term rental investment in Nashville has historically concentrated in several redevelopment corridors surrounding the downtown core. These neighborhoods offered a combination of zoning eligibility, redevelopment opportunity, and practical rideshare access to the Lower Broadway entertainment district, which made them attractive locations for purpose-built STR communities.

However, while many projects between 2021 and 2024 were developed in these surrounding corridors, recent investor interest in 2025 and into 2026 has increasingly shifted toward locations closer to downtown. As the market matures, proximity to the entertainment district and convention activity is becoming an even more important factor in property performance.

Several neighborhoods have played particularly important roles in Nashville’s STR development cycle.

North Nashville, 37207

North Nashville emerged as one of the most active STR development corridors during the expansion phase of the market. Located just north of downtown, the area offered redevelopment parcels that could support clusters of purpose-built townhome communities while still providing relatively quick rideshare access to the entertainment district.

Land economics, zoning eligibility, and development scale all aligned in this corridor, which helped attract several large STR communities during the early growth phase of the market.

Music Row and Edgehill, 37203

The Music Row and Edgehill corridor sits immediately south of downtown and remains one of the most strategically located areas for STR ownership. Properties in this area benefit from extremely close proximity to the downtown entertainment district, Music City Center, and several of the city’s major tourism drivers.

Because of that locational advantage, pricing in this corridor can be higher than in surrounding redevelopment areas. However, the closer proximity to downtown has increasingly attracted investor attention as the market evolves.

West Nashville, 37209

West Nashville has also emerged as an important STR development corridor, particularly for investors seeking purpose-built townhome product with convenient access to downtown. The area benefited from redevelopment opportunities that allowed developers to build larger communities during the expansion phase of the market.

Although it sits slightly farther from the entertainment district than some other corridors, West Nashville still offers practical rideshare access to downtown while supporting redevelopment-oriented housing formats.

Market Interpretation

During the expansion phase of the Nashville STR market, many developments were concentrated in redevelopment corridors surrounding downtown where land availability and zoning allowed larger projects to be built. As the market matures, however, investor attention is gradually shifting toward properties located closer to the downtown entertainment district, where proximity to tourism activity can provide a competitive advantage.

Understanding this geographic shift is important for investors evaluating both existing properties and future development opportunities in the Nashville STR market.

11. The Two Nashville STR Markets

Nashville’s Airbnb sector is increasingly best understood as 2 distinct short-term rental markets, each driven by different types of properties, guest behavior, and competitive dynamics.

The Condo STR Market

The first segment consists primarily of studio, 1 bedroom, and 2 bedroom condominium units located in or near the downtown core. These properties depend heavily on walkability, high occupancy levels, and nightly rates that remain competitive with nearby hotels.

In the earliest phase of Nashville’s STR expansion, these units were among the most common investment properties. However, the operating environment for this segment has evolved. Downtown Nashville has experienced significant hotel development during the past decade, and many of these hotels offer amenities such as rooftop bars, restaurants, and concierge services that small STR units cannot easily replicate.

As a result, condo-style STR properties now compete more directly with the hospitality sector, particularly in locations where hotel inventory has grown rapidly.

The Purpose-Built Townhome STR Market

The second segment consists of larger purpose-built STR homes, most commonly four-bedroom townhomes designed to host groups of visitors. These properties typically include multiple sleeping areas, rooftop entertainment space, and open layouts that support group travel.

Rather than competing directly with hotels, these properties serve a different category of demand. Many visitors traveling to Nashville arrive in groups for events such as bachelor and bachelorette parties, concerts, sporting events, and conventions. Larger STR homes allow these groups to stay together in a single property, which often provides both convenience and cost advantages compared with booking multiple hotel rooms.

Because this segment targets group-oriented travel demand, it generally faces less direct competition from traditional hotels and has often demonstrated stronger revenue potential under current market conditions.

Market Interpretation

Understanding the distinction between these two segments is one of the most important analytical frameworks for evaluating the Nashville STR market. Investors who treat all short-term rental properties as interchangeable often misinterpret both pricing and performance trends.

Condo STR economics and purpose-built townhome economics operate under different competitive dynamics. In the current market environment, purpose-built townhome properties designed for group travel sit at the center of Nashville’s STR investment landscape.

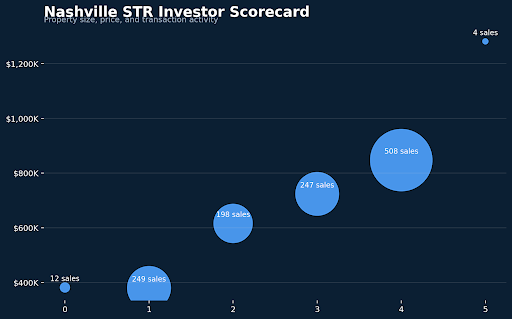

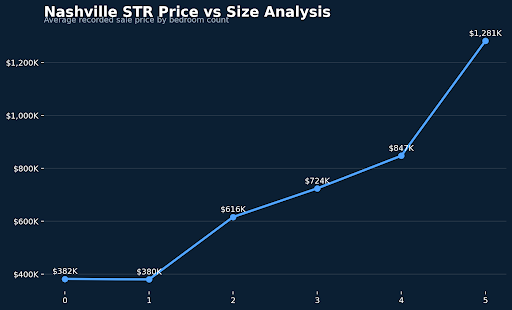

12. Revenue Benchmarks and Property Performance

The following ranges reflect typical annual revenue patterns observed across Nashville STR properties during recent market cycles.

|

Property Type |

Typical Annual Revenue |

|

Studio / 1 bedroom condo |

$40,000 to $65,000 |

|

2 bedroom STR property |

$55,000 to $80,000 |

| 3 bedroom STR home |

$75,000 to $110,000 |

|

4 bedroom STR townhome |

$110,000 to $170,000+ |

These figures represent typical operating ranges rather than guaranteed performance, and individual property results can vary depending on location, management quality, seasonality, and market conditions.

These benchmarks reflect the underlying demand structure of the Nashville tourism economy. Visitors frequently travel to the city in groups for bachelor and bachelorette parties, sporting events, concerts, festivals, and conventions. As a result, properties capable of accommodating larger groups tend to capture stronger booking demand.

This dynamic explains why the largest revenue gap in the table occurs not between one and two bedroom properties, but between smaller units and the fully group-oriented four bedroom townhome product.

Key Takeaway

4 bedroom STR homes sit at the center of the Nashville market, combining strong revenue potential with high levels of investor participation.

Market Interpretation

These revenue patterns do not simply describe the market. They help explain why the Nashville STR sector evolved the way it did. Developers responded to group-oriented travel demand by building larger properties designed specifically for short-term rental use. Investors followed the revenue potential associated with those properties. The result was the emergence of purpose-built STR communities anchored by four bedroom, four bathroom townhomes designed to host larger groups of visitors.

13. Typical Nashville Airbnb Operating Costs

Revenue is only half the investment equation. Operating costs matter, and out-of-state investors often underestimate them.

The most common expense categories include cleaning and turnover, utilities, internet, maintenance, insurance, furnishing refresh, platform fees, and property management if used.

Cleaning is often one of the largest and most variable costs because STR properties turn over frequently. Utilities are usually higher than in traditional long-term rentals because guests use the home intensively and occupancy may be continuous during peak seasons. Insurance can also be meaningfully more expensive than standard landlord coverage.

For investors who do not self-manage their properties, professional property management services represent another major expense category. In Nashville, management fees typically range from 15% to 23% of gross rental revenue, depending on the scope of services provided and the operational complexity of the property.

Market Interpretation

The strongest Nashville STR properties are not just the ones with high gross revenue. They are the ones whose revenue is strong enough to absorb the real operating complexity of short-term rental ownership. Larger, group-oriented homes often have an advantage here because their revenue scale can support these costs more comfortably.

14. Nashville STR Financing Environment

Financing short-term rental properties often differs from financing traditional residential real estate in several important ways.

While some investors still use conventional mortgage products when available, many STR acquisitions are financed through debt service coverage ratio (DSCR) loans, portfolio lending, or other investor-oriented financing structures. DSCR loans evaluate a property’s ability to generate sufficient income to cover its debt obligations rather than focusing primarily on the borrower’s personal income.

This structure places greater emphasis on expected rental performance, including occupancy assumptions, seasonal demand, and projected nightly rates. As a result, underwriting quality can vary depending on how lenders interpret the revenue potential of a particular property.

Down payment requirements also tend to be higher than in traditional owner-occupied financing. Many STR investors contribute 20% to 30% equity at acquisition, particularly when purchasing non-owner-occupied properties or purpose-built STR homes.

Interest rate conditions also influence the investment landscape. Higher borrowing costs can reduce speculative demand and place greater emphasis on properties with durable revenue potential.

Market Interpretation

Financing structure shapes who can compete in the Nashville STR market. Because many of the most desirable properties are purpose-built townhomes or newly constructed communities with relatively high purchase prices, capital structure often matters almost as much as location. In the current environment, well-capitalized buyers with flexible financing options frequently hold a competitive advantage.

15. Nashville STR Tax Advantages for Investors

Tax treatment is one reason short-term rental properties continue to attract sophisticated real estate investors.

Recent federal tax legislation restored 100% bonus depreciation for certain qualifying property components, allowing investors to deduct a substantial portion of depreciation in the first year a property is placed into service. In practice, this often occurs through a cost segregation study, which identifies portions of a property that qualify for accelerated depreciation schedules.

For investors with sufficient taxable income, this structure can significantly increase the value of first-year depreciation deductions associated with a newly acquired STR property.

Short-term rentals may also receive different passive-activity treatment than traditional long-term rental properties under certain circumstances. According to IRS Publication 925, activities with an average customer use period of 7 days or less are not treated as rental activities for passive-activity purposes. Publication 925 also outlines several material participation tests, including the commonly referenced 100-hour participation threshold combined with more participation than any other individual involved in the activity.

For some investors, the interaction between accelerated depreciation and material participation rules can meaningfully influence the after-tax return profile of a short-term rental investment.

Market Interpretation

Although tax considerations should never be the sole reason to acquire an investment property, the potential for accelerated depreciation and favorable participation treatment has played an important role in attracting capital to the Nashville STR market. Investors evaluating these opportunities should consult qualified tax professionals to determine how these rules apply to their specific circumstances.

16. Nashville STR Zoning, Regulation, and Permitting

Nashville’s STR market exists within a defined regulatory framework, and investors who do not understand that framework are at a disadvantage.

Metro Nashville distinguishes between owner-occupied and not-owner-occupied short-term rental permits and requires owners to obtain an operating permit. Metro’s permit pages explain that not-owner-occupied permits are only issued where allowed by zoning, and that permits for specific plan or planned unit development properties must also be allowed by the governing plan documents. Metro also renews STR permits annually.

That means investors must think about two layers of viability:

- Can the property legally support the intended STR use under zoning and governing plan conditions?

- Can the owner obtain and maintain the required permit?

Metro’s permit application process also requires proof of ownership, specific documentation, and in the case of not-owner-occupied permits, additional records linking the individual applicant to an entity when ownership is held in an LLC or similar structure. Metro’s checklist further notes proof of taxes, insurance, floor plans, and an affidavit for not-owner-occupied applications.

Grant Hammond has worked closely with investors and engaged in discussions with local officials on these issues, which matters because the technical side of STR ownership often determines whether a deal is truly viable.

17. Pricing Stability, Developer Incentives, and Effective Pricing

Recorded sale prices suggest that Nashville STR pricing has remained relatively stable during the past two years. In a headline sense, that observation is correct. However, it does not fully capture how transactions are being structured in the current market environment.

In many newly completed developments, developers have chosen to maintain published asking prices while increasing buyer incentives designed to support transaction activity. These incentives can include closing cost credits, furnishing allowances, interest rate buydowns, HOA dues credits, or flexible closing timelines.

The result is a meaningful distinction between headline pricing and effective pricing.

Developers often prefer to protect comparable sales by maintaining list prices that support valuations for current and future projects. At the same time, offering incentives allows them to improve the economics of a transaction without formally lowering the recorded sale price.

Investor Insight

Many newly constructed STR developments in Nashville are maintaining list prices while offering meaningful buyer incentives. Investors evaluating these opportunities should focus not only on the recorded sale price but also on the effective acquisition cost, which reflects the real economics of the transaction after incentives are considered.

Market Interpretation

This dynamic is one of the clearest indicators that the Nashville STR market has transitioned into a more disciplined investment environment. Prices may not be falling dramatically, but negotiating leverage has shifted. Investors who evaluate effective pricing and negotiate strategically can often secure more favorable deal structures than were available during the expansion phase of the early 2020s.

18. The Nashville STR Supply Pipeline

A meaningful amount of short-term rental inventory was delivered in Nashville between 2021 and 2025 as developers responded to the rapid expansion phase of the market.

Projects across North Nashville, Edgehill, Music Row, West Nashville, and several surrounding redevelopment corridors introduced new STR communities designed primarily around townhome-style product and group-oriented travel demand. This wave of development expanded the available inventory of investment properties while also increasing competition in certain submarkets.

Looking forward, several structural forces are likely to shape the pace of future STR development.

Zoning Constraints

Nashville’s zoning framework continues to limit where non-owner-occupied STR properties can legally operate. Over time, regulatory changes have narrowed the geographic areas where investor-oriented developments can be built, which naturally restricts the number of viable development sites.

Construction Costs

Construction costs remain meaningfully higher than they were prior to the pandemic-era building cycle. Higher labor costs, material prices, and financing expenses all influence the feasibility of new development projects, particularly for communities designed specifically for STR use.

Financing Conditions

Financing conditions for speculative development are also more conservative than during the low interest rate period that supported the early expansion of the Nashville STR market. Developers must now evaluate projects under more disciplined lending assumptions, which can reduce the number of projects that move forward.

Taken together, these constraints suggest that the pace of new STR supply may slow compared with the rapid development cycle between 2021 and 2025.

Market Interpretation

The largest wave of new STR supply may already have been delivered. That does not mean new projects will disappear, but it does suggest that future development may become more selective. For investors, that dynamic can support the long-term competitiveness of well-located existing properties if tourism demand remains strong and the pipeline of new competing inventory moderates.

19. How Nashville Compares to Other Inland STR Markets

When evaluating Nashville’s short-term rental market, it is useful to compare the city not with traditional vacation destinations such as beach or mountain markets, but with other inland cities where tourism, events, and entertainment drive visitor demand.

Cities such as Austin, Charlotte, Indianapolis, and Atlanta provide useful reference points. Each of these markets benefits from population growth, professional sports, event activity, and urban tourism. However, Nashville’s STR market developed somewhat differently because of the unique structure of the city’s entertainment economy.

Austin shares several similarities with Nashville, including strong population growth, a nationally recognized music identity, and a tourism economy tied to festivals and entertainment. However, Austin’s STR regulatory framework has historically been more complex and restrictive, which has shaped the development of its short-term rental market.

Charlotte benefits from professional sports and corporate travel demand, but much of its visitor traffic is tied to business travel rather than leisure-driven tourism. As a result, Charlotte’s accommodation demand tends to be more hotel-oriented and less centered on large group travel.

Indianapolis generates strong tourism during major sporting events and conventions, but that demand tends to be more episodic. The city’s visitor economy is less consistently tied to leisure travel than Nashville’s music and entertainment-driven tourism.

Atlanta is a much larger metropolitan area with a diverse visitor economy. However, tourism activity is more geographically dispersed across the city, which creates a more decentralized STR market compared with Nashville’s highly concentrated entertainment district.

Market Interpretation

Among major inland cities, Nashville is distinctive because it combines a concentrated entertainment core, strong leisure-driven tourism demand, and a development model that embraced purpose-built STR communities at scale. That combination has helped position Nashville as one of the most visible and active inland short-term rental investment markets in the United States.

20. Why Nashville Attracts Out-of-State Investors

Out-of-state investors have played a significant role in the growth of Nashville’s short-term rental market. A meaningful share of buyers acquiring STR properties in recent years have come from outside Tennessee, particularly from large metropolitan areas where investors are already familiar with tourism-driven real estate.

Several structural characteristics of the Nashville market help explain this pattern.

Demand

The first factor is the strength and visibility of Nashville’s tourism economy. The city attracts millions of visitors annually and has developed a national reputation as a destination for music, entertainment, conventions, and large group celebrations. For investors evaluating markets from a distance, Nashville’s demand profile is relatively easy to understand compared with cities where tourism drivers are less obvious.

Predictability

The second factor is geographic clarity. Because so much visitor activity is concentrated around Lower Broadway and the downtown entertainment district, it is easier for non-local investors to evaluate what constitutes a strong location. Properties located within a short rideshare distance of the entertainment core generally capture the majority of visitor demand, which simplifies location analysis.

Tax Environment

The third factor is Tennessee’s broader tax environment. Tennessee does not impose a traditional wage income tax, and the state has long maintained a reputation as a relatively investor-friendly jurisdiction. While tax treatment varies depending on individual circumstances, this broader perception contributes to Nashville’s appeal among out-of-state buyers evaluating multiple markets.

Product Transparency

Finally, Nashville’s growing inventory of purpose-built STR communities provides investors with a clearer operating framework than markets dominated by scattered individual properties. Many developments feature standardized layouts, consistent design features, and operational structures that make it easier for investors to evaluate expected performance.

Market Interpretation

Taken together, these factors help explain why Nashville has become one of the most visible inland STR investment markets in the United States. The city combines strong tourism demand, a concentrated entertainment district, relatively transparent product types, and an investment environment that outside buyers can evaluate with a reasonable degree of confidence.

21. The Nashville STR Investment Environment in 2026

The Nashville STR market in 2026 is meaningfully different from the expansion-driven market that existed in 2021. The current environment is more selective, more rational, and in many cases more favorable to disciplined buyers.

Several factors have contributed to this shift. Higher interest rates have reduced speculative investor demand compared with the early expansion phase of the market. At the same time, new inventory delivered between 2022 and 2025 has expanded the range of available properties, giving buyers more options than were available during the height of the acquisition cycle. In addition, continued hotel development in the downtown core has introduced additional competition for smaller STR units, particularly studio and one-bedroom condominiums.

Developers have responded to these conditions in several ways. In many cases, projects continue to maintain headline pricing while offering buyer incentives designed to support transaction momentum. These incentives can include closing cost credits, furnishing packages, HOA concessions, or interest rate buydowns that reduce the effective acquisition cost for investors.

Investor Insight

In practical terms, the Nashville STR market in 2026 often functions as a buyer-friendly acquisition environment, especially when compared with the highly competitive expansion period of the early 2020s. Investors who focus on effective pricing, revenue durability, zoning clarity, and long-term location quality can frequently negotiate stronger terms than were available when investor demand was at its peak.

Market Interpretation

A more rational market environment is not a negative development for experienced investors. In early-stage expansion cycles, momentum can drive pricing and decision-making. In more mature markets, property fundamentals become more important. Nashville’s STR sector appears to be entering that stage. The market continues to benefit from long-term structural demand tied to tourism and entertainment activity, but investors now have greater opportunity to apply disciplined underwriting and selective acquisition strategies.

22. What Makes a Successful Nashville Airbnb Investment

After more than 1,200 Nashville STR transactions, several patterns appear consistently among the strongest properties.

Property Size

Guest capacity is one of the most important drivers of STR performance in Nashville. Properties with 4 bedrooms and 4 bathrooms have become the dominant investment format because they accommodate the group-oriented travel patterns that define much of Nashville’s tourism demand. Bachelor and bachelorette parties, sports weekends, and concert travel frequently involve multiple guests traveling together, making larger homes significantly more competitive than smaller units.

Rooftop Entertainment Space

Rooftop decks have become one of the defining architectural features of many Nashville STR properties. In practice, these spaces function as an extension of the guest experience. Properties with rooftop gathering areas, skyline views, or outdoor entertaining space often command stronger booking demand because they provide a social environment that traditional hotel rooms cannot replicate.

Proximity to Downtown

It’s a return to the most basic fundamentals: location remains the most durable driver of STR performance. Properties located within a short rideshare distance of the downtown entertainment district tend to achieve stronger occupancy and pricing power because visitors typically spend a significant portion of their trip near Lower Broadway, major music venues, and event destinations.

Purpose-Built Design

Properties designed specifically for short-term rental use generally outperform homes that were originally built for traditional residential occupancy. Purpose-built STR communities often incorporate layouts that accommodate multiple sleeping areas, open gathering spaces, and design features that support frequent guest turnover.

Market Interpretation

Successful Nashville STR investments rarely depend on a single attribute. Instead, the strongest properties typically combine location, guest capacity, entertainment-oriented design, and operational practicality. Investors who focus on how visitors actually experience Nashville often identify opportunities that may be less obvious when evaluating properties through a purely residential real estate lens.

23. What Investors Should Watch Next

As the Nashville short-term rental market moves deeper into a more disciplined investment environment, several forward-looking indicators will play an outsized role in shaping the next phase of the market.

For investors evaluating Nashville over the next 12 to 36 months, 4 signals deserve especially close attention.

Zoning and Policy

Future regulatory changes remain one of the most important variables in the Nashville STR market. Additional adjustments to zoning rules or permit structures could further narrow, redefine, or concentrate the areas where investor-owned short-term rental properties can legally operate. For that reason, policy risk should remain a core part of acquisition underwriting, particularly for buyers evaluating new construction or redevelopment-oriented opportunities.

Hotel Supply

Hotel competition is most relevant for smaller STR units, especially studio and 1 bedroom properties that compete directly with traditional hotel rooms. Continued hotel development in and around downtown Nashville should therefore be monitored closely, particularly in submarkets where walkability to Lower Broadway is a major part of the value proposition. Larger group-oriented STR properties are less directly exposed, but the broader growth of hospitality supply still influences pricing psychology across the market.

Development Pipeline

Although Nashville experienced a substantial wave of STR development between 2021 and 2025, several structural constraints may limit the pace of future supply. Zoning restrictions have narrowed the areas where investor-owned STR properties can operate, construction costs remain elevated relative to pre-pandemic levels, and financing conditions are more conservative than during the low-rate expansion period. Taken together, these factors suggest that future STR development may become more selective rather than disappearing entirely. That could benefit well-located existing properties if demand remains healthy and new competing inventory becomes harder to deliver.

Tourism Growth

The most important long-term variable remains Nashville’s visitor economy. As long as the city continues to attract strong music, event, convention, and sports-related traffic, the core demand story for short-term rentals remains intact. Nashville’s tourism base is broad enough that it does not rely on a single event category or seasonal driver, which continues to support long-term structural demand for accommodations near the city’s entertainment core.

Market Interpretation

Investors do not need every variable to move in their favor at once. They need to understand which variables matter most. In Nashville, the next phase of the STR market will likely be shaped less by speculation and more by a combination of policy clarity, selective new supply, tourism durability, and disciplined acquisition strategy.

24. Data Sources, Methodology, and Limitations

This report is based primarily on analysis of more than 1,200 publicly recorded Nashville short-term rental property transactions occurring between 2020 and 2025.

The dataset provides insight into investor acquisition activity, pricing trends, geographic concentration, and the broader evolution of the Nashville STR investment market during this period.

However, the dataset should not be interpreted as a complete inventory of every operating Airbnb property in Nashville. Some STR properties were constructed and retained by developers, some were converted to short-term rental use without a recorded sale, and some transfers occurred through private transactions that may not appear in typical MLS-based datasets.

As a result, the transaction data analyzed in this report is best understood as a detailed study of publicly recorded STR investment acquisitions, rather than a full census of all STR properties operating in Davidson County.

In addition to transaction-level analysis, operational observations throughout this report are informed by market participation through more than 550 Nashville STR transactions represented by Grant Hammond, as well as direct familiarity with development patterns, investor underwriting criteria, zoning considerations, and buyer behavior across multiple phases of the market cycle.

Market Interpretation

No single dataset can fully eliminate uncertainty in a rapidly evolving real estate market. However, analysis grounded in transaction data, development history, and hands-on market participation provides a significantly stronger foundation for investor decision-making than generalized market commentary alone.