Fannie Mae condo financing restrictions tightened significantly during the housing downturn, creating new challenges for condo buyers, developers, and urban residential projects across the country.

According to reporting published by RTTNews and The Wall Street Journal, Fannie Mae increased the minimum sold threshold for condominium projects from 51% to 70% before backing mortgage financing within a building.

These changes had major implications for projects within the Nashville real estate market, particularly newer high-rise developments that were still early in their sales cycles.

Additional reporting from The Wall Street Journal highlighted how these restrictions added pressure to already struggling condo developments during the housing downturn.

Fannie Mae Condo Financing Restrictions Tighten

The updated guidelines introduced several stricter financing requirements. Condo projects now needed at least 70% of units sold before qualifying for broader Fannie Mae-backed financing.

The previous benchmark had been 51%, making the new threshold substantially harder to achieve.

Fannie Mae also restricted financing in buildings where association fee delinquencies exceeded 15% or where a single entity owned more than 10% of units.

Why These Changes Mattered

Condo financing availability directly affects transaction volume. When financing becomes more restrictive, buyer pools shrink quickly.

Projects still working through early absorption phases faced the greatest pressure. Buyers who relied on conventional financing suddenly had fewer available options.

Developers argued that these restrictions could slow housing recovery efforts by limiting financing access at a time when the market already faced weak demand.

Impact on Nashville Condo Developments

Several Nashville condo projects were likely affected by the higher sold threshold. Developments such as 5th & Main, Rolling Mill Hill, Velocity, Rhythm, and Terrazzo were all competing within a challenging financing environment.

Projects that could not meet financing benchmarks often had to pursue alternative strategies. Some shifted units into rentals, reduced pricing aggressively, or explored seller financing structures.

This pattern aligns with broader housing market trends, where tighter financing standards can materially slow absorption and pricing recovery.

Higher Down Payment Requirements Add More Pressure

At the same time, condo buyers with less than 25% down faced additional fees. This increased transaction costs for many purchasers, even those with strong credit profiles.

Combined with tighter project eligibility standards, these rules created another hurdle for both developers and buyers during an already fragile period for urban housing markets.

What This Still Tells Us About Condo Markets

Condo markets are highly sensitive to financing conditions. Changes in lending standards can quickly affect pricing, inventory absorption, and overall project stability.

Understanding financing thresholds remains critical when evaluating urban residential developments, especially during periods of economic stress.

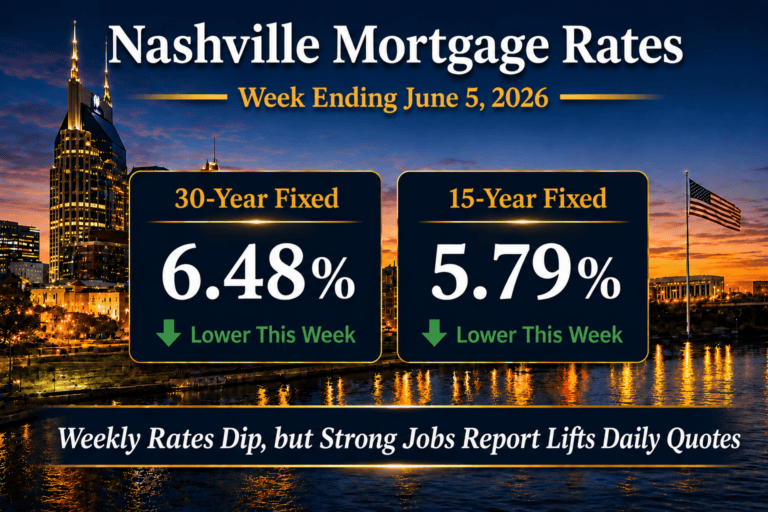

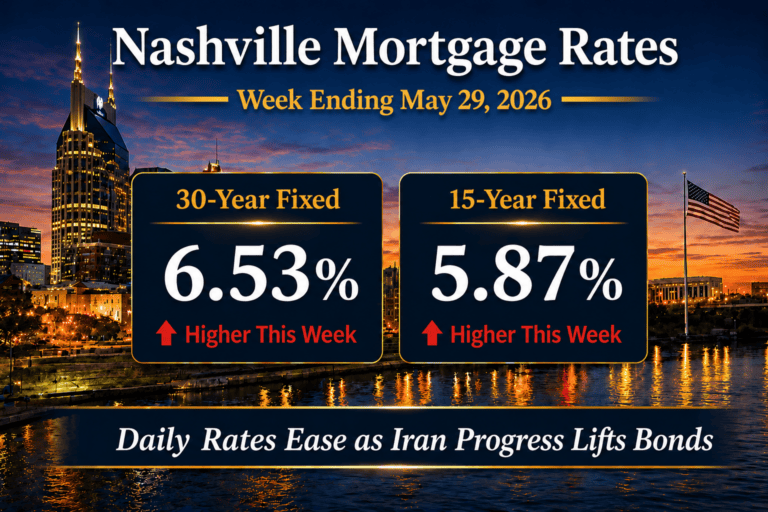

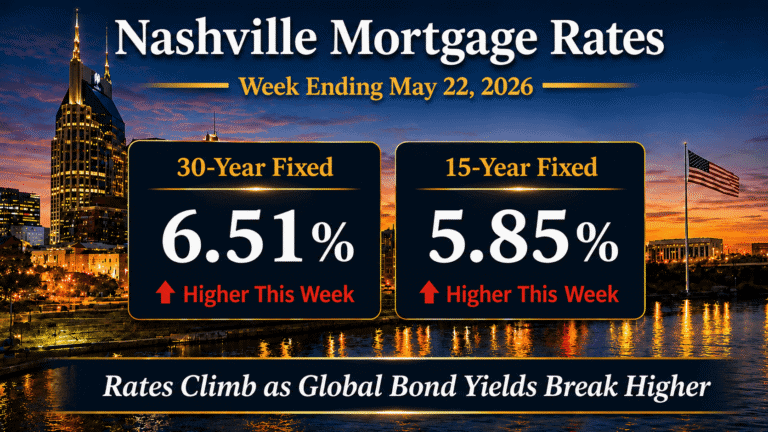

For more financing insights, explore Nashville mortgage rates and financing.

August 12, 2009, 5:38 am

I understand that both ICON and Velocity have somehow been able to retain their FHA approval (I’m guessing based on their early contract numbers). I’ve been told that FHA trumps Fannie Mae in some lender’s eyes. Terrazzo has gained preliminary Fannie Mae approval dues to it’s green qualities – they’re just waiting on paperwork. 5th & Main is attempting to fill itself with “lease-purchase” agreements in an attempt to get back into FHA’s good graces. I’m betting that RMH will try the same thing. But I agree, I’ve had to learn a lot more about financing than I used to need to know.

August 11, 2009, 10:38 pm

I understand that both ICON and Velocity have somehow been able to retain their FHA approval (I’m guessing based on their early contract numbers). I’ve been told that FHA trumps Fannie Mae in some lender’s eyes. Terrazzo has gained preliminary Fannie Mae approval dues to it’s green qualities – they’re just waiting on paperwork. 5th & Main is attempting to fill itself with “lease-purchase” agreements in an attempt to get back into FHA’s good graces. I’m betting that RMH will try the same thing. But I agree, I’ve had to learn a lot more about financing than I used to need to know.

August 12, 2009, 5:55 am

In the condo world FHA insured money seems to be king since their guidelines only require 51% of a project to be under contract whereas Fannie and Freddie are 70% plus they fee you to death. Here is a REALLY nice tool that the gov’t gives us to see if a condo project is FHA approved: https://entp.hud.gov/idapp/html/condlook.cfm

You’ll notice that 5th & Main’s FHA status is “rejected”…oops.

August 11, 2009, 10:55 pm

In the condo world FHA insured money seems to be king since their guidelines only require 51% of a project to be under contract whereas Fannie and Freddie are 70% plus they fee you to death. Here is a REALLY nice tool that the gov’t gives us to see if a condo project is FHA approved: https://entp.hud.gov/idapp/html/condlook.cfm

You’ll notice that 5th & Main’s FHA status is “rejected”…oops.

August 14, 2009, 5:08 pm

September 14, 2009, 5:31 pm