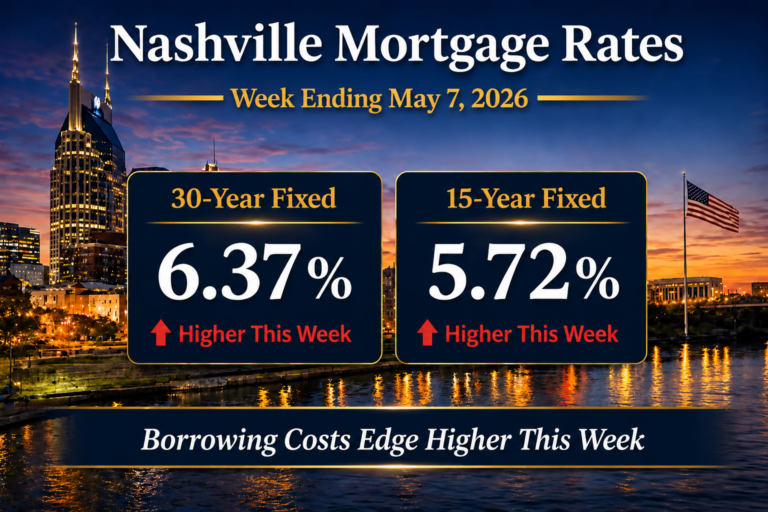

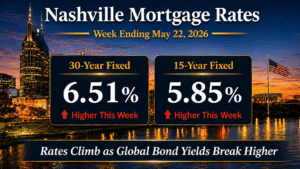

Nashville mortgage rates averaged 6.51% for the 30-year fixed and 5.85% for the 15-year fixed for the week ending May 22, 2026, according to Freddie Mac’s Primary Mortgage Market Survey. Rates pushed to fresh 2026 highs this week. Global bond markets repriced sharply higher. The 10-year Treasury yield climbed back to 4.60%. That level has acted as a ceiling several times over the past few years. Meanwhile, the 30-year jumped 15 basis points week over week. The 15-year rose 14 basis points. Overall, this was the largest weekly increase since the early-year repricing.

Domestic data did not drive this week’s move. Instead, oil traded near $100 per barrel. The Iran conflict remained unresolved. Meanwhile, global sovereign yields ran sharply higher alongside U.S. Treasuries. For example, Japan’s 10-year bond yield hit a 1996 high. The UK’s 30-year gilt yield reached a 1998 high. Germany’s 30-year bund yield climbed to a 2011 high. Daily lender quotes were also more volatile than the weekly Freddie Mac average suggests. In fact, quotes spiked on Tuesday to a nine-month high. They recovered modestly into Friday. As a result, borrowers in Nashville and Middle Tennessee saw meaningfully different rate sheets depending on which day they locked.

For Davidson County and Williamson County buyers active in the spring market, I see this as the rate environment testing the upper edge of the range I have been tracking in our latest Nashville mortgage rate updates for the past two months. Several factors will decide which way rates move next. First, the 4.60% ceiling on the 10-year. Second, the Memorial Day holiday-shortened trading week ahead. Third, Federal Reserve Chair Kevin Warsh’s first full week. Finally, the Core PCE inflation print due Friday. Together, these signals will determine which side of the range rates settle into over the next four to six weeks.

In this report

Market Summary

- Nashville 30-year fixed mortgage rate averaged 6.51%, up from 6.36% last week.

- Nashville 15-year fixed mortgage rate averaged 5.85%, up from 5.71% last week.

- FHA 30-year mortgage rates were near 6.30%.

- The 10-year Treasury yield ended near 4.60%, up from 4.46% the prior week.

- Mortgage spreads were near 1.91%, or 191 bps.

- Federal Reserve policy remained restrictive, with the Fed Funds rate at 3.50% to 3.75% and Kevin Warsh’s first full week as Fed Chair beginning May 26.

- MBA mortgage applications fell 2.3% in the week ending May 15, with purchase applications down 4% week over week but still 8% above the same week one year ago. The refinance share of total applications climbed to 41.9%.

- Core CPI ran at 2.8% year over year in the April release, up from 2.6% in March.

According to Freddie Mac PMMS, the 30-year fixed climbed 15 basis points in a single week, the largest one-week jump since the early-year repricing. Both the 30-year and 15-year remain below year-ago levels of 6.86% and 6.01% respectively, though the year-over-year discount has compressed sharply over the last three weeks.

Mortgage Rate Dashboard

The mortgage rate dashboard shows a 6.51% 30-year fixed rate, a 5.85% 15-year fixed rate, an FHA 30-year rate near 6.30%, a 10-year Treasury yield near 4.60%, and a mortgage spread near 1.91%.

Nashville Mortgage Rates This Week

For the week ending May 22, 2026, the 30-year fixed averaged 6.51%. The 15-year averaged 5.85%. Both moved meaningfully higher. Specifically, the 30-year rose 15 basis points week over week. The 15-year rose 14 basis points. This was the largest weekly move higher since the early-year repricing. Moreover, it reversed the multi-week descent that had carried the 30-year as low as 6.23% on April 24.

Year over year, the picture remains favorable. The 30-year sits 35 basis points below last year’s 6.86% reading. Similarly, the 15-year is 16 basis points below last year’s 6.01%. However, the year-over-year discount has compressed over the past three weeks. That is because headline rates have moved higher while year-ago comparisons stayed roughly flat.

This week’s volatility was the highest since late March. Daily lender quotes pushed to a nine-month high on Tuesday. Global sovereign bond yields broke out together. Then quotes eased through Wednesday and Thursday. Headlines pointed toward improved Iran de-escalation prospects. By Friday’s close, daily rates were back near the prior Friday’s level. However, that level was itself already a nine-month high. The Freddie Mac PMMS weekly average captured the elevated zone. Importantly, it smoothed across the intraweek range.

For Middle Tennessee buyers active across Davidson and Williamson Counties, the lock window matters more this week than usual. In fact, the spread between the best and worst lock day was wider than at any point in the past two months. MBA mortgage application volume confirmed the demand-side response. Total applications fell 2.3% on a seasonally adjusted basis for the week ending May 15. Purchase applications dropped 4% week over week. Still, purchase activity remains 8% above the same week one year ago. Meanwhile, the refinance share of total applications climbed to 41.9%.

Institutional Macro Snapshot

What Is Driving Mortgage Rates Right Now?

1. Treasury yields are setting the base rate

The 10-year Treasury closed the week at 4.60%. That is an increase of roughly 14 basis points from the prior Friday. Thursday’s session high reached 4.62%. The move was concentrated rather than gradual. In fact, Tuesday accounted for most of the weekly change. Meanwhile, global sovereign yields broke higher together. Investors priced in continued inflation risk. They also priced in rising government debt loads. Furthermore, unresolved geopolitical pressure in the Middle East tied to the Iran conflict added pressure. Oil traded near $100 per barrel. As a result, oil feeds the headline inflation calculation. It also raises the cost of every input across the broader economy. Importantly, mortgage pricing tracks the 10-year much more closely than the federal funds rate. Therefore, the move flowed through almost in full to the rates Nashville buyers saw at lock. This follows a similar pattern to our May 1 Nashville mortgage rate update, when the prior Treasury repricing also flowed through one-for-one to PMMS within the same week.

2. Mortgage spreads are shaping borrower pricing

The spread between the 30-year fixed and the 10-year Treasury held at approximately 191 basis points this week. That is essentially unchanged from the prior week. Through 2025 and early 2026, spread compression had been one of the cleanest pieces of good news for borrowers. Specifically, spreads ground back from the historically elevated 230 to 250 basis point band of 2023. Now they sit in the 175 to 200 basis point range that approximates a normal market. Importantly, this week’s flat spread reading is preferable to a scenario where both Treasuries and spreads widened together. It means the entire move in the headline mortgage rate came from Treasuries. As a result, mortgage-backed securities pricing did not deteriorate. Still, spreads remain wider than the pre-2022 long-run average of 150 to 170 basis points. However, they are materially narrower than the 2023 peak.

3. Federal Reserve policy is keeping the rate floor elevated

The federal funds rate remains at 3.50% to 3.75% after the April 29 hold. Meanwhile, the market-implied probability of a 2026 rate cut continued to fade this week. Core CPI ticked up to 2.8% in the April BLS release. Global yields also broke higher. Additionally, Kevin Warsh begins his first full week as Federal Reserve Chair on Monday, May 26. Markets will pay close attention to his tone on inflation. They will also watch his framing of the current rate environment. The dot plot from March 2026 indicated a tilt toward a 25-basis-point cut this year. However, that path now requires one of two things. First, a meaningful drop in oil and inflation expectations. Second, a dovish tone shift from the new chair. Neither is the base case today.

The 10-Year Treasury and Mortgage Rate Spreads

The 10-year Treasury is the primary benchmark for long-term mortgage rate direction. The mortgage rate borrowers actually receive depends on the spread between mortgage rates and Treasury yields.

This week, the spread was approximately 1.91%. The math reflects a 6.51% Freddie Mac 30-year fixed rate and a 4.60% 10-year Treasury yield. That figure is essentially unchanged from the prior week’s 191 bps. For context, pre-2022 long-run averages ran between 150 and 170 basis points. As a result, spreads remain wider than historical norms. Still, they are materially narrower than the 2023 peak of 230 to 250 basis points.

Two drivers shape the spread. The first is interest-rate volatility. When the bond market becomes choppier, mortgage-backed securities investors demand a wider spread. This compensates them for prepayment risk and duration uncertainty. This week’s Tuesday spike pushed implied volatility higher temporarily. However, it eased through Wednesday and Thursday. That is why the spread did not widen meaningfully despite the Treasury move. The second driver is institutional demand for MBS. Importantly, MBS demand has held up despite the global yield repricing.

Mortgage rates can fall even when Treasury yields hold steady. That happens as long as spreads compress. In fact, that mechanism powered most of the rate improvement through 2024 and the first quarter of 2026. However, spreads now sit near the lower end of the normalized range. As a result, the next leg of rate improvement requires Treasury yields to fall. Spreads cannot tighten much further from here. That is a meaningful shift in where the next 25 to 50 basis points of relief has to come from.

Payment Impact for Nashville Buyers

This week’s PMMS 30-year rate moved from 6.36% to 6.51%. The locked payment scenario uses a $400,000 loan amount, which corresponds to a $500,000 purchase price with 20% down, a 30-year fixed-rate amortization, and excludes property taxes, homeowner’s insurance, HOA dues, and PMI.

- $400,000 loan at 6.51% (this week): Principal and interest are approximately $2,531 per month.

- $400,000 loan at 6.36% (last week): Principal and interest were approximately $2,492 per month.

- Week-over-week change: Approximately $39 higher per month.

- 30-year lifetime impact of this week’s 15-basis-point increase: Approximately $14,165 in additional interest over the full loan term at this loan size.

- Year-over-year comparison: Versus the 6.86% rate one year ago on May 22, 2025, the same buyer pays approximately $93 less per month, or roughly $1,114 less per year.

For Nashville’s most rate-sensitive segments, this matters most in the entry-level band. A $39 monthly payment increase is small in absolute terms, but at the margin it pushes some buyers across their debt-to-income ceiling on the property they had targeted. Two additional Nashville loan tiers for context, using the same amortization assumptions:

- $750,000 loan (typical $937,500 home with 20% down): At 6.51%, principal and interest are approximately $4,745 per month. That is $74 higher than at last week’s 6.36% rate and $174 less than at last year’s 6.86% rate.

- $1,000,000 loan (typical $1,250,000 home with 20% down): At 6.51%, principal and interest are approximately $6,327 per month. That is $98 higher than at last week’s rate and $232 less than at last year’s rate.

The year-over-year improvement is still real, but the compression of that improvement over the last three weeks changes the planning calculus for any buyer who has been waiting. A buyer who would have paid $2,617 per month at the April 24 low of 6.23% on a $400,000 loan is now paying $2,531 at 6.51%, which is $86 more per month than they would have locked four weeks ago.

Strategic Borrower Considerations in Today’s Market

I read this week as the rate environment testing the upper edge of the range that has held since early March. Specifically, the 10-year is sitting at a multi-year technical ceiling. Meanwhile, the Iran headlines could resolve in either direction. Friday’s Core PCE inflation print is coming. So are Fed Chair Warsh’s first policy signals. Both will land in the next two weeks. Until those data points print, posture matters more than prediction.

- Buyers who have identified the right property and can pencil the payment at 6.51% should focus on the property and the lock window rather than waiting for a hoped-for rate retracement. The next data points that could move rates meaningfully lower are still two to four weeks away, and the path between now and then is more likely sideways-to-up than down.

- Sellers in the under-$1 million band should expect price-reduction frequency to climb as the rate move filters through. Builder-side data shows roughly 32% of new construction listings nationally took a price reduction in May at an average of 6%. The resale side mirrors that pattern with a lag, and Nashville’s spring inventory has been building across Davidson and Williamson Counties.

- Investors running cash flow on short-term rental or DSCR purchases should rerun the numbers at current rate levels. The DSCR market typically prices 0.5 to 1.0 percentage points above primary-residence conforming rates, which puts current DSCR pricing in the 7.0% to 7.5% band. Spread compression on the institutional side has lagged the headline mortgage market, so DSCR pricing is more sensitive to this kind of volatility week.

- Move-up buyers carrying a low-rate first mortgage face a sharper trade-off than they did three weeks ago. The cost of giving up a sub-5% existing rate to buy at 6.51% requires meaningful equity, a meaningful upgrade, or a meaningful change in living needs to pencil. Builder-paid 2-1 rate buydowns on new construction are increasingly common in the Middle Tennessee suburbs including Brentwood, Franklin, and the Williamson County corridor, and worth running as part of any move-up comparison.

Grant Hammond has 25 years of Nashville real estate experience and has closed over $1 billion in career sales across Davidson and Williamson Counties, including more than 100 luxury transactions above $1.5 million, more than 350 downtown Nashville high-rise condominium transactions, and more than 550 short-term rental transactions where financing structures, including DSCR loans and rate-sensitive investor purchases, were central to the deal.

In Grant’s experience across multiple Nashville rate cycles, weeks like this one (where the 10-year Treasury tests a multi-year technical level after a geopolitical shock) tend to resolve within three to four weeks. Either the 4.60% level acts as a ceiling and yields fade back toward 4.30%, or it breaks decisively and the next leg targets the 4.85% to 5.00% band. Grant has watched Nashville’s payment-sensitive entry-level segment respond fastest to whichever way that resolution lands, with the East Nashville and Germantown markets showing the most immediate buyer-side sensitivity, followed by the Green Hills and Brentwood mid-market band.

Nashville Real Estate Market Outlook

My base case for Nashville mortgage rates over the next four to six weeks is straightforward. The 30-year fixed will likely trade between 6.40% and 6.70%. That assumes the 10-year Treasury holds between 4.45% and 4.65%. It also assumes mortgage spreads remain near 190 basis points. However, the Memorial Day holiday-shortened week ahead carries several catalysts. Consumer Confidence lands Tuesday. The second estimate of Q1 GDP arrives Thursday. Core PCE inflation prints Friday. Furthermore, Treasury auctions of 2-year, 5-year, and 7-year notes are spaced through the week. Finally, Kevin Warsh’s first full week as Fed Chair adds an additional layer of tone-and-framing watching.

If Friday’s Core PCE confirms the Core CPI acceleration to 2.8% and Iran headlines stay unresolved, the 30-year could press toward 6.65% to 6.85% over the next four to six weeks. Treasury auction demand would be the early signal, with weak demand pushing yields through the 4.60% technical ceiling and strong demand defending it. If Core PCE softens and de-escalation headlines firm up, the 30-year could retrace toward 6.20% to 6.40% as the Treasury market unwinds the inflation and geopolitical premium it added this week.

For Nashville specifically, two segments remain the most rate-sensitive. The under-$500,000 entry-level segment in Davidson County and the $500,000 to $1 million band that spans East Nashville, Germantown, parts of Green Hills, and the Brentwood feeder communities absorb the largest activity response to a 25 to 50 basis point move in either direction. Both are now seeing the early-stage drag of this week’s move, though the late-week recovery off Tuesday’s daily-lender peak limited the damage to actual contracts that printed before Friday. The luxury market above $1.5 million is far less rate-sensitive. Cash buyers, jumbo financing relationships, and portfolio loan structures dominate that segment, and Nashville luxury inventory has held its pricing power through the spring even as broader inventory has loosened.

For a sense of how the spread mechanics work in the opposite direction, our April 24 Nashville mortgage rate update tracks the multi-week descent from the April highs to the early-May lows. The same mechanics work in reverse, which is what this week showed, and the full library is available in the Mortgage Rates and Financing category.

Forward-looking statements in this post reflect current data, cited forecasts, and our team’s interpretation of market conditions as of May 22, 2026. Future performance may differ materially. This is not investment advice. Grant Hammond is a Tennessee-licensed broker (#261980) at Compass RE.

Nashville Mortgage Rates FAQ

What are Nashville mortgage rates today?

Nashville mortgage rates averaged 6.51% for the 30-year fixed and 5.85% for the 15-year fixed for the week ending May 22, 2026, according to the Freddie Mac PMMS benchmark. The 30-year rose 15 basis points and the 15-year rose 14 basis points week over week. Both rates remain below year-ago levels of 6.86% and 6.01% respectively, though the year-over-year discount has compressed sharply over the last three weeks.

Did mortgage rates go up or down this week?

Nashville mortgage rates rose this week, with the 30-year fixed up 15 basis points and the 15-year fixed up 14 basis points on a weekly average basis per Freddie Mac. Daily lender pricing was more volatile, spiking on Tuesday to a nine-month high before recovering modestly into Friday’s close. The week ended at elevated levels but without a fresh peak above Tuesday’s intraweek high.

Why did mortgage rates move this week?

The 10-year Treasury yield climbed 14 basis points to 4.60% as global sovereign bond yields broke higher together and oil traded near $100 per barrel on unresolved Iran conflict tensions. Japan, the UK, and Germany all saw multi-decade highs in their long-duration government bond yields. Mortgage rates tracked Treasuries almost one-for-one because mortgage spreads stayed essentially flat at 191 basis points, so the entire move flowed through directly to borrowers.

How does the 10-year Treasury affect mortgage rates?

The 10-year Treasury is the primary benchmark for 30-year fixed mortgage pricing, with mortgage-backed securities investors pricing relative to the 10-year and the spread between the two currently near 191 basis points. When Treasury yields rise, mortgage rates typically rise by a similar amount within a few business days. This week, the 10-year rose roughly 14 basis points and the 30-year mortgage rose 15 basis points, which is a near one-for-one passthrough.

Are Nashville mortgage rates expected to fall in 2026?

The Federal Reserve’s March 2026 dot plot indicated a tilt toward a 25-basis-point reduction this year, though the market-implied probability of that cut has faded after this week’s global yield move and the Core CPI acceleration to 2.8%. The path forward depends on three things: Iran de-escalation that brings oil prices lower, a Core PCE inflation print that confirms or contradicts the recent acceleration, and the tone Federal Reserve Chair Kevin Warsh sets in his first weeks on the job. If those line up favorably, the 30-year could retrace toward 6.20% to 6.40%.

Should Nashville buyers wait for lower mortgage rates?

For Nashville buyers who have identified the right property and can pencil the payment at 6.51%, waiting carries meaningful opportunity cost because the next rate-moving data points are two to four weeks away and the trajectory between now and then is more likely sideways-to-up than down. Davidson and Williamson County spring inventory has been building, which gives buyers negotiating room on price and concessions that may offset part of the rate move. Builder-paid 2-1 rate buydowns on new construction are increasingly common in the Middle Tennessee suburbs and worth running as part of any timing comparison.