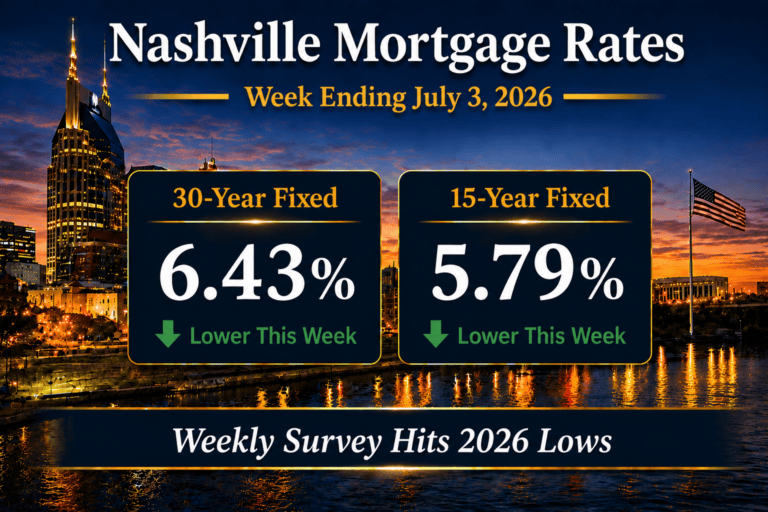

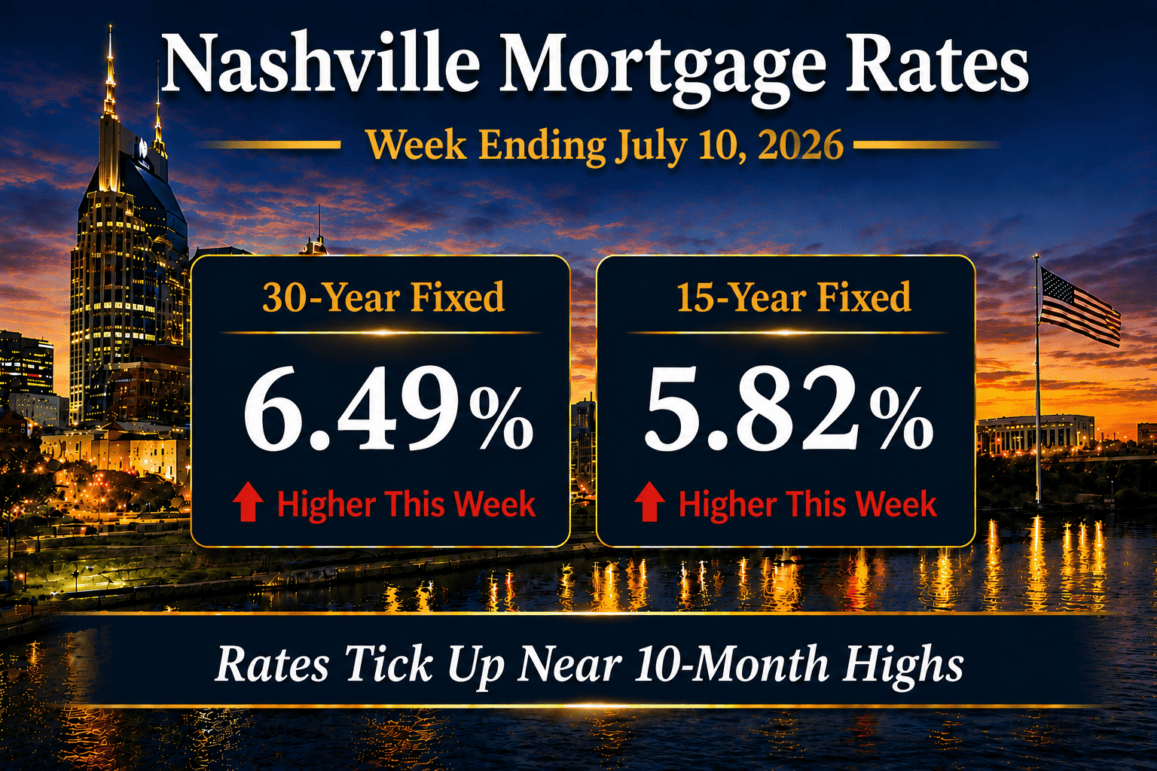

Nashville mortgage rates averaged 6.49% for the 30-year fixed and 5.82% for the 15-year fixed for the week ending July 10, 2026, according to Freddie Mac PMMS. Both rose modestly week over week, the 30-year up 6 basis points from 6.43% and the 15-year up 3 basis points from 5.79%, leaving survey rates near their highest levels in ten months.

The driver this week was oil. The end of the U.S. and Iran ceasefire pushed crude prices higher, and a bond market with little new data of its own was content to follow oil along for the ride. Higher fuel prices imply higher inflation, and higher inflation tends to pull rates up with it. The one wrinkle came Friday, when Treasury yields kept drifting higher even as oil eased, most likely as traders positioned for next week’s testimony from Fed Chair Kevin Warsh and two key inflation reports. In the bigger picture, mortgage rates are drifting sideways in a fairly narrow range, but it is a range sitting near the 10-month highs.

For Middle Tennessee buyers, a 6 basis point move does not change the payment math much on its own, but the direction matters when rates are already testing the top of their recent range. I update our Nashville mortgage rate tracker every week so buyers and sellers across Davidson and Williamson Counties can see where financing conditions stand before they make a decision.

In this report

Market Summary

- Nashville 30-year fixed mortgage rate averaged 6.49%, up from 6.43% the prior week

- Nashville 15-year fixed mortgage rate averaged 5.82%, up from 5.79% the prior week

- FHA 30-year mortgage rates were near 6.23%

- The 10-year Treasury yield ended near 4.55%, up about 9 basis points on the week

- Mortgage spreads were near 1.94%, or 194 bps, down about 3 bps

- Federal Reserve policy remained restrictive, with the federal funds rate held at 3.50% to 3.75%

- MBA mortgage applications fell 2.2% for the week ending July 3, 2026, a holiday-week blip, with purchase applications running about 5% ahead of a year ago and refinance applications about 8% ahead

Weekly averages come from the Freddie Mac PMMS release for the week ending July 10, 2026.

Mortgage Rate Dashboard

The mortgage rate dashboard shows a 6.49% 30-year fixed rate, a 5.82% 15-year fixed rate, an FHA 30-year rate near 6.23%, a 10-year Treasury yield near 4.55%, and a mortgage spread near 1.94%.

Nashville Mortgage Rates This Week

Both benchmark rates rose this week. The 30-year fixed averaged 6.49%, up from 6.43% the prior week, and the 15-year fixed averaged 5.82%, up from 5.79%. Year over year the 30-year sits 18 basis points below the same week in 2025, while the 15-year is essentially flat, 2 basis points above where it was a year ago.

Daily lender pricing told a slightly different story than the weekly survey. The Mortgage News Daily 30-year index eased to 6.65% by Thursday after approaching 10-month highs midweek, a modest recovery that tracked oil finally moving lower. The weekly Freddie Mac average, which smooths the daily noise, still printed higher because it captured the earlier run-up.

For Nashville buyers the practical read is that financing costs held near the top of their recent band rather than breaking out of it. I am watching whether next week’s inflation reports and the Warsh testimony push the range or simply hold it.

Institutional Macro Snapshot

What Is Driving Mortgage Rates Right Now?

Three forces moved rates this week, and all three point back to the same question the bond market keeps asking: where is inflation headed.

Oil prices and the end of the U.S. and Iran ceasefire

The end of the U.S. and Iran ceasefire was the week’s big story for oil, and crude prices spiked. Because fuel is central to inflation, and inflation is central to rates, the bond market followed oil higher. The oil and rate relationship is never perfect, but with little other data to trade on, bonds were willing to be taken along for the ride.

The 10-year Treasury and Fed Funds Futures repricing

The 10-year Treasury ended the week near 4.55%, and Friday brought a small divergence worth noting: yields kept drifting higher even as oil eased on the day. Fed Funds Futures moved even more sharply than longer-term Treasuries, which points to traders repricing the near-term policy path rather than reacting to oil alone.

Positioning ahead of Warsh testimony and two inflation reports

The simplest read on Friday’s drift is positioning. Fed Chair Kevin Warsh testifies before Congress next week, and two inflation reports print in the same window: the June Consumer Price Index on July 14, 2026, and the June Producer Price Index on July 15, 2026. When the calendar is that heavy, traders tend to move ahead of the data rather than wait for it.

The 10-Year Treasury and Mortgage Rate Spreads

The 10-year Treasury ended the week near 4.55%, up about 9 basis points from 4.46% a week earlier. The 30-year fixed rose only 6 basis points over the same stretch, so the spread between the two narrowed to roughly 1.94%, or 194 basis points, down from 197 basis points the prior week.

The spread is the gap between the 30-year fixed and the 10-year Treasury, and it reflects how efficiently the mortgage-backed securities market is pricing risk. A spread near 194 basis points is still wide by long-run standards, which means there is room for mortgage rates to improve even if the Treasury holds steady, provided the bond market calms down.

This week the spread narrowed for a mechanical reason more than a healthy one: the Treasury rose faster than the mortgage rate. Bonds had little data of their own to trade on and largely followed oil, so the modest spread tightening is worth watching but not yet worth celebrating.

Payment Impact for Nashville Buyers

At the current 6.49% 30-year fixed rate, principal and interest on a $500,000 loan runs about $3,157 a month. On a $1,000,000 loan it is about $6,314. A half-point move in either direction shifts the $500,000 payment by roughly $160 a month and the $1,000,000 payment by roughly $330, which is the practical reason a 6 basis point weekly move matters more for direction than for this month’s budget.

For investors, the math reads differently. Buyers shopping for East Nashville rental and short-term rental product are underwriting to cash flow, not just to a payment, and at these rates the deals that pencil are the ones bought right rather than the ones financed cheaply. I track that segment closely alongside the East Nashville homes for sale as it moves.

The band I guide most Middle Tennessee buyers to right now is simple: qualify at today’s rate, not at the rate you hope to refinance into. If rates improve later, a refinance is a bonus, not the plan.

Strategic Borrower Considerations in Today’s Market

With rates near the top of their recent range, the borrowers who do best are the ones who separate the rate decision from the house decision. The right house at a slightly higher rate beats the wrong house at a slightly lower one, and rate locks give you a floor while you shop.

Builder buydowns and seller concessions remain the most reliable way to cut the effective rate on new construction across Williamson County and the Middle Tennessee suburbs. When a builder offers to buy the rate down, run the math on the permanent buydown against a price reduction of the same dollar cost, because the better deal depends on how long you plan to hold the loan.

For anyone weighing a 15-year against a 30-year, the 67 basis point gap between 5.82% and 6.49% this week is real money over the life of the loan, but only if the higher 15-year payment fits comfortably. Most of my clients use the 30-year for flexibility and simply pay it down faster when they can.

Nashville Real Estate Market Outlook

The next Federal Reserve meeting runs July 28 to 29, 2026, with the federal funds rate held at 3.50% to 3.75%. Before that, Fed Chair Kevin Warsh testifies before Congress next week and two inflation reports print, the June Consumer Price Index on July 14, 2026, and the June Producer Price Index on July 15, 2026, any of which can move the 10-year Treasury and local rates with it.

On jobs, the June employment report already released on July 2, and it produced a bond-specific reaction that had nothing to do with oil. The next Employment Situation report, covering July, is due August 7, 2026, so the labor-market catalyst sits on the far side of the Fed meeting rather than in the week ahead.

Locally, demand is firmer than the headlines suggest. The latest MBA survey showed total applications down 2.2% for the holiday week ending July 3, but purchase applications are running about 5% ahead of a year ago and refinance applications about 8% ahead. For Nashville and Middle Tennessee sellers, that is the number that matters: buyers are still in the market at these rates.

Nashville Mortgage Rates FAQ

What are Nashville mortgage rates today?

For the week ending July 10, 2026, the 30-year fixed averaged 6.49% and the 15-year fixed averaged 5.82%, per Freddie Mac PMMS. Both rose slightly from the prior week, the 30-year up 6 basis points and the 15-year up 3 basis points. Daily lender pricing sat a bit higher, near 6.65% on the Mortgage News Daily index.

Did Nashville mortgage rates go up or down this week?

They went up modestly. The 30-year fixed rose from 6.43% to 6.49% and the 15-year fixed rose from 5.79% to 5.82%. The move was driven by higher oil prices after the end of the U.S. and Iran ceasefire, which pulled the bond market and mortgage rates up with it.

Why do oil prices affect mortgage rates?

Fuel is a large component of inflation, and inflation is the single biggest driver of long-term interest rates. When oil spikes, bond investors expect higher inflation and demand higher yields, which pushes the 10-year Treasury and mortgage rates higher. The link is not perfect, but it has been strong through much of 2026.

What is the mortgage spread and why does it matter?

The mortgage spread is the difference between the 30-year fixed rate and the 10-year Treasury yield, near 194 basis points this week. A wide spread means mortgage rates carry an extra risk premium over Treasuries, so there is room for rates to fall if the bond market stabilizes, even without help from the Fed.

How much does a rate change affect a Nashville mortgage payment?

At 6.49% on a $500,000 loan, principal and interest run about $3,157 a month. A half-point rate change moves that payment by roughly $160 a month. On a $1,000,000 loan the payment is about $6,314, and a half-point change moves it by roughly $330.

Will Nashville mortgage rates fall in 2026?

Rates are drifting sideways near 10-month highs rather than trending down, and the next moves depend on inflation data and Federal Reserve policy. The Fed meets July 28 to 29, 2026, with the funds rate held at 3.50% to 3.75%. Forecasts are not guarantees, and daily quotes depend on your credit profile, loan size, and property type.

Sources and methodology

Rate data in this update reflects weekly averages from the Freddie Mac Primary Mortgage Market Survey (PMMS) for the week ending July 10, 2026. Daily lender pricing context is sourced from the Mortgage News Daily Mortgage Rate Index. Macro indicators including the 10-year Treasury yield reference Federal Reserve Economic Data (FRED) series DGS10. Spread analysis between mortgage rates and the 10-year Treasury uses the PMMS minus DGS10 series. Application volume references the Mortgage Bankers Association Weekly Applications Survey. Year-over-year comparisons reference the same Freddie Mac PMMS week from the prior year.

- Freddie Mac Primary Mortgage Market Survey (PMMS): https://www.freddiemac.com/pmms (retrieved July 10, 2026)

- Mortgage News Daily Mortgage Rate Index: https://www.mortgagenewsdaily.com/mortgage-rates (retrieved July 10, 2026)

- FRED DGS10, 10-Year Treasury Constant Maturity Rate (Board of Governors of the Federal Reserve System): https://fred.stlouisfed.org/series/DGS10 (retrieved July 10, 2026)

- Federal Reserve H.15 Selected Interest Rates (10-year Treasury daily close): https://www.federalreserve.gov/releases/h15/ (retrieved July 10, 2026)

- Federal Reserve FOMC calendar (next meeting July 28 to 29, 2026): https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm (retrieved July 10, 2026)

- U.S. Bureau of Labor Statistics, Employment Situation schedule (next release August 7, 2026): https://www.bls.gov/schedule/news_release/empsit.htm (retrieved July 10, 2026)

- U.S. Bureau of Labor Statistics, Consumer Price Index (May 2026 release, Core CPI YoY): https://www.bls.gov/cpi/ (retrieved July 10, 2026)

- Mortgage Bankers Association Weekly Applications Survey (week ending July 3, 2026): https://www.mba.org/news-and-research (retrieved July 10, 2026)

About the broker. Grant Hammond is a Tennessee-licensed real estate broker at Compass RE with 25 years of Middle Tennessee brokerage experience and over $1 billion in career closings.

Commission and compensation disclosure. Broker fees are not set by law and are fully negotiable. There is no standard or going rate. All commission and buyer-agency details should be discussed and agreed in writing before contract. This disclosure is provided for transparency and is not an offer of specific terms.

Rate disclosure. Mortgage rates change daily. The rates referenced above are the Freddie Mac PMMS weekly average for the week ending July 10, 2026. Daily lender quotes will differ based on credit profile, loan size, property type, and lock period. Nothing in this analysis constitutes a rate lock guarantee or a commitment to lend. Speak with a licensed mortgage professional for personalized pricing.

Forward-looking statement. Any outlook on rates, inflation, Federal Reserve policy, or the Nashville real estate market reflects observations as of July 10, 2026, and is subject to change without notice. Forecasts are not guarantees. This post is informational and is not financial, legal, or tax advice.