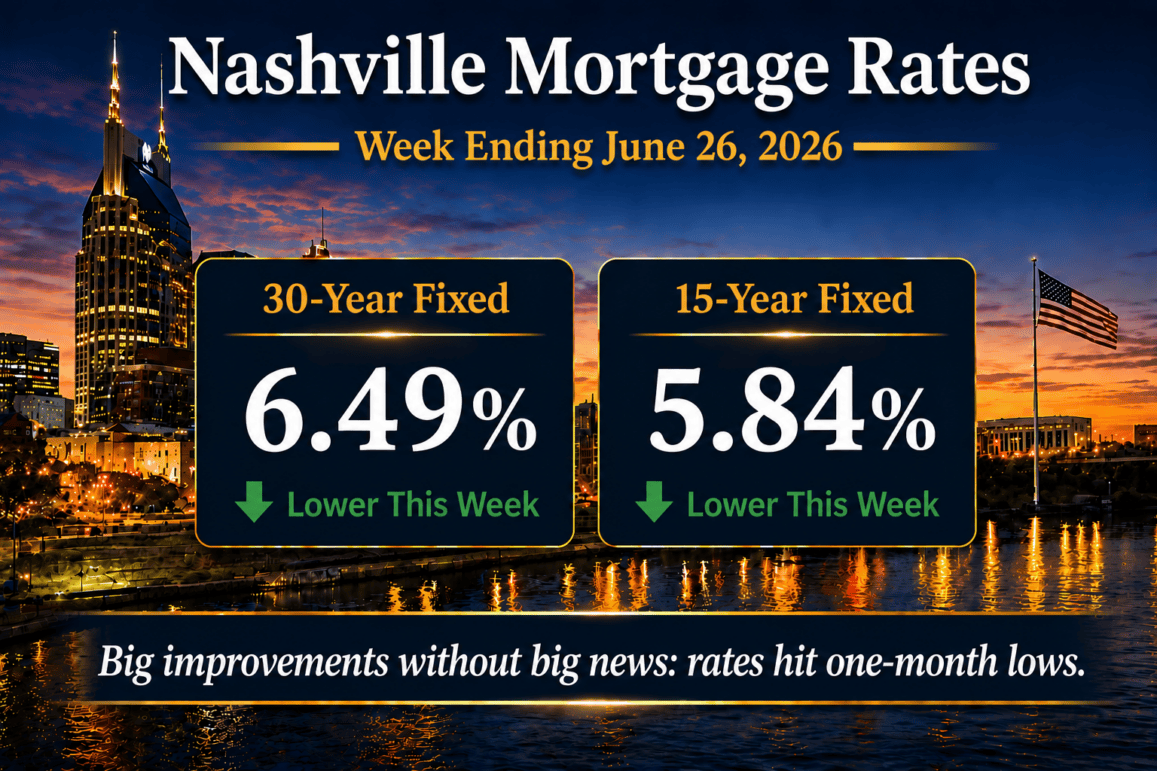

Nashville mortgage rates averaged 6.49% on the 30-year fixed and 5.84% on the 15-year fixed for the week ending June 26, 2026, according to Freddie Mac PMMS. Both edged up marginally, the 30-year by 2 basis points and the 15-year by 3, even as the 10-year Treasury eased to roughly 4.38%.

As Jeff Beck put it, “I’m going down, down, down, down, down.” That was the week for rates, and the fun part is it happened without a single dramatic headline. Two forces did the work: crude oil slid back toward $70 a barrel as Iran tensions eased, easing the inflation outlook, and quarter-end rebalancing pushed institutions to buy bonds. More demand for bonds means lower yields, and daily lender pricing finished at its lowest level since mid-May.

I publish this read every Friday because the gap between the daily headline rate and what actually clears at the closing table matters for Middle Tennessee buyers. For the live weekly snapshot, see our Nashville mortgage rate tracker; this post is the broker read on what moved and what it means locally.

In this report

Market Summary

- Nashville 30-year fixed mortgage rate averaged 6.49%, up from 6.47% the prior week (up 2 basis points).

- Nashville 15-year fixed mortgage rate averaged 5.84%, up from 5.81% the prior week (up 3 basis points).

- FHA 30-year mortgage rates were near 6.10%.

- The 10-year Treasury yield ended near 4.38%, down from about 4.43% the prior week.

- Mortgage spreads were near 2.11%, or 211 basis points, up about 7 basis points on the week.

- Federal Reserve policy remained restrictive, with the federal funds rate held at 3.50% to 3.75% at the June 16 to 17 meeting.

- Year over year, the 30-year is down 28 basis points (from 6.77%) and the 15-year is down 12 basis points (from 5.96%).

The weekly averages above come from the Freddie Mac PMMS release for the week ending June 26, 2026. Daily lender pricing context references the Mortgage News Daily rate index.

Mortgage Rate Dashboard

The mortgage rate dashboard shows a 6.49% 30-year fixed rate, a 5.84% 15-year fixed rate, an FHA 30-year rate near 6.10%, a 10-year Treasury yield near 4.38%, and a mortgage spread near 2.11% (211 bps).

Nashville Mortgage Rates This Week

Nashville mortgage rates improved this week even though the weekly survey barely moved, and I watch both numbers because they told two different stories. The Freddie Mac average landed at 6.49% on the 30-year and 5.84% on the 15-year, each a marginal 2 to 3 basis points above the prior week. After drifting toward recent highs early on, daily lender pricing recovered sharply Wednesday and held through Friday at the lowest levels since mid-May.

The two numbers diverge because the weekly survey still carries Monday’s and Tuesday’s weakness, while the daily index caught the late-week rally. Year over year, the 30-year is down about 28 basis points from 6.77% and the 15-year about 12.

For the buyers I am working with across Davidson and Williamson Counties, the practical read is that the lock window got better as the week went on, the kind of move that rewards being underwritten and ready.

Institutional Macro Snapshot

What Is Driving Mortgage Rates Right Now?

Three forces set the rate this week, and none was a dramatic headline. Energy prices fell, the 10-year Treasury continued a six-week downtrend, and quarter-end positioning added a bid for bonds. That is calmer than recent weeks, when a single news event drove the tape, a dynamic I covered in last week’s Nashville mortgage rate update.

1. Treasury yields are setting the base rate

The 10-year Treasury eased to about 4.38%, extending a six-week decline from a brief 4.69% high. Falling oil and quarter-end bond buying did the work, and the tell was that the Wednesday move arrived with no headline and no reaction in Fed Funds Futures, the signature of technical buying. The 10-year is the base rate every Nashville mortgage is built on, so when it falls, the local floor drops with it.

2. Mortgage spreads are shaping borrower pricing

The spread between the 30-year fixed and the 10-year widened to about 211 basis points, up roughly 7 on the week, since the survey ticked up while the 10-year fell. That still sits well above the 170 to 180 of a calmer market, so a tightening spread could lower Nashville rates even if Treasuries hold here. It is the variable I am watching most closely.

3. Federal Reserve policy is keeping the rate floor elevated

The Fed held at 3.50% to 3.75% on June 16 to 17, and Chair Kevin Warsh has given no reason to price a near-term cut. The fading oil shock helps him, since it eases the risk of an inflation reacceleration that would force another hike. The next meeting is July 28 to 29, but the nearer catalyst is next week’s labor data, and I am watching whether it gives the Fed cover to soften its tone.

The 10-Year Treasury and Mortgage Rate Spreads

The spread is the gap between the 30-year fixed and the 10-year Treasury. This week it ran about 2.11%, or 211 basis points (6.49% minus 4.38%), up roughly 7 basis points from the prior week’s 204 basis points.

The trend is the friend here. Six weeks ago the 10-year was at 4.69%; this week it sat near 4.38%, and that steady decline has done more for borrowers than any single session. A footnote worth keeping: the last time the 10-year held above 4.60% for a full 90 days was 2008, a reminder of how hard it is for long-term yields to stay elevated. The one offset is the widening spread, since the mortgage market has not fully passed the Treasury improvement through yet.

Nashville mortgage rates can fall even when Treasury yields are flat, because a tightening spread does the work, and with the spread still wide there is room for that if MBS demand firms.

Payment Impact for Nashville Buyers

At this week’s 6.49% 30-year rate, principal and interest on a $500,000 loan runs about $3,157 a month, up roughly $7 from the prior week. A marginal move.

On a $1,000,000 loan, common in the Williamson County and luxury segments I work in, principal and interest at 6.49% runs about $6,314 a month. At this size, the buyers I represent watch builder concessions and rate buydowns closely, since on new construction those move the effective payment more than a 2 basis point survey tick ever will.

For investors weighing short-term rental acquisitions, financing costs still sit above the long-run norm. The East Nashville market remains a focus for buyers running these numbers, where the entry price changes the payment calculus relative to the downtown core. This week’s improvement helps at the margin, but a 211 basis point spread is the number I tell investors to underwrite to.

Strategic Borrower Considerations in Today’s Market

With the spread wide and the 10-year trending lower, the borrowers who win are positioned to lock on a daily dip rather than wait for the weekly average. This week made the point: daily pricing hit its lowest since mid-May on Wednesday and Thursday, well before the survey caught up.

The band I guide buyers to is simple. Get fully underwritten before you shop, so a rate dip is something you can act on inside a day. The daily-versus-weekly gap this week is the whole argument for being ready before the move, not after.

A 15-year at 5.84% against a 30-year at 6.49% is also a real fork for buyers with the cash flow to carry the higher payment. For the right balance sheet, that 65 basis point gap is worth a hard look.

Nashville Real Estate Market Outlook

Because of the July 4 holiday, the June jobs report moves up to Thursday, July 2, and the bond market is closed Friday, July 3. It is the most likely near-term catalyst to move the 10-year and, with it, Nashville mortgage rates: a hot payroll number could stall this week’s improvement, while a soft one would let the downtrend run. It is a busy data week otherwise, with JOLTS, ADP, ISM Manufacturing, jobless claims, and Consumer Confidence all due, and no Fed speeches or Treasury auctions to compete, so the data takes center stage.

The next Fed meeting is July 28 to 29, but with the funds rate at 3.50% to 3.75% and Warsh leaning hawkish, the market is not pricing a near-term cut. For the broader local picture, see our Nashville market analysis. Congress also passed a housing package this week aimed at supply and affordability. It will not change inventory overnight, but more supply over time is healthy for buyers and a more balanced market.

My read for Middle Tennessee buyers and sellers: treat any further dip as a gift from quarter-end positioning rather than a new trend, since most of that tailwind has likely blown through. If you are close to a decision, this is a good window to get your financing buttoned up. And if you want my read on a specific purchase or listing, that conversation is usually faster than another lap through the rate headlines.

Nashville Mortgage Rates FAQ

What are Nashville mortgage rates today?

For the week ending June 26, 2026, Nashville mortgage rates averaged 6.49% on the 30-year and 5.84% on the 15-year, per Freddie Mac PMMS, with FHA near 6.10%. Daily lender quotes vary by credit profile, loan size, and property type.

Did Nashville mortgage rates go up or down this week?

On the weekly average they edged up 2 to 3 basis points, a marginal move. Daily lender pricing actually improved into the end of the week on an on-target PCE print, reaching the lowest levels since mid-May before the weekly average caught up.

Why did the spread widen if the 10-year Treasury fell?

The 10-year fell about 5 basis points to 4.38% while the weekly mortgage average rose 2, so the spread widened to about 211 basis points. The weekly survey lags daily market moves, which is part of why the two diverged.

What is the mortgage spread and why does it matter?

It is the difference between the 30-year fixed and the 10-year Treasury, about 211 basis points this week (6.49% minus 4.38%), and it reflects the efficiency of the mortgage-backed securities market. When it tightens, Nashville mortgage rates can fall even if Treasury yields hold flat.

When is the next event that could move rates?

The June jobs report releases Thursday, July 2 (moved up for the July 4 holiday, with the bond market closed Friday, July 3), and the next Fed meeting runs July 28 to 29. The jobs data is the more important near-term driver for rates.

How much would a $500,000 loan cost per month at today’s rate?

At 6.49%, principal and interest on a $500,000 loan is about $3,157 a month, and a $1,000,000 loan about $6,314. Taxes, insurance, and HOA dues are additional, and daily lender pricing will vary.

Sources and methodology

Rate data reflects weekly averages from the Freddie Mac PMMS for the week ending June 26, 2026. Daily lender pricing comes from the Mortgage News Daily rate index. The 10-year Treasury references FRED series DGS10, cross-checked against the Mortgage News Daily reference, and the spread is PMMS minus DGS10. Payment figures use the standard principal-and-interest amortization formula. Year-over-year comparisons use the same Freddie Mac PMMS week a year earlier.

- Freddie Mac Primary Mortgage Market Survey (PMMS), week ending June 26, 2026: https://www.freddiemac.com/pmms (retrieved June 26, 2026)

- Mortgage News Daily rate index, daily 30-year, 15-year, FHA, and jumbo lender pricing: https://www.mortgagenewsdaily.com/mortgage-rates (retrieved June 26, 2026)

- FRED DGS10, 10-year Treasury Constant Maturity Rate (Board of Governors of the Federal Reserve System): https://fred.stlouisfed.org/series/DGS10 (retrieved June 26, 2026)

- Federal Reserve H.15 Selected Interest Rates (10-year Treasury daily close): https://www.federalreserve.gov/releases/h15/ (retrieved June 26, 2026)

- Federal Reserve FOMC calendar (June 16 to 17 meeting; next meeting July 28 to 29, 2026): https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm (retrieved June 26, 2026)

- U.S. Bureau of Labor Statistics, Employment Situation schedule (June 2026 reference month releases July 2, 2026): https://www.bls.gov/schedule/news_release/empsit.htm (retrieved June 26, 2026)

- U.S. Bureau of Labor Statistics, Consumer Price Index (May 2026 release, Core CPI YoY): https://www.bls.gov/cpi/ (retrieved June 26, 2026)

- Mortgage Bankers Association, Weekly Applications Survey: https://www.mba.org/news-and-research/research-and-economics/single-family-research/weekly-applications-survey (retrieved June 26, 2026)

Verified broker authority: 25 years of Middle Tennessee brokerage and over $1 billion in career closings at Compass RE.

Commission and compensation disclosure: Broker fees are not set by law and are fully negotiable. There is no standard or going commission rate. All commission and buyer-agency details should be discussed before contract. This applies to all representation by Grant Hammond at Compass RE.

Mortgage rates change daily. The rates referenced above are the Freddie Mac PMMS weekly average for the week ending June 26, 2026. Daily lender quotes will differ based on credit profile, loan size, property type, and lock period. Nothing in this analysis constitutes a rate lock guarantee or a commitment to lend. Speak with a licensed mortgage professional for personalized pricing.

Forward-looking statement: Any commentary on the direction of rates, Treasury yields, Federal Reserve policy, or the Nashville real estate market reflects observations as of June 26, 2026, and is not a forecast or a guarantee. Markets can move quickly and unpredictably. Make financing and real estate decisions based on conditions at the time of your transaction, not on this analysis.