East Nashville | Cumberland River corridor across from Downtown Nashville

CMA Fest is the single most predictable demand event on the Nashville short-term rental calendar. The Country Music Association’s flagship festival runs June 4 to June 7 in 2026 and typically delivers four nights of high-occupancy, premium-priced bookings concentrated within roughly two miles of the downtown core. The week leading into the festival is when STR operators finalize pricing, when investors decide whether to deploy capital before the summer ramp, and when the booking data tells you what the rest of the summer will look like.

This is a category post for the Nashville Airbnb silo. It covers what STR investors should watch the week of May 28 through June 3, what the booking data is telling me about the festival window itself, and what the broader resale market looks like for STR-eligible product inside a 6-mile downtown radius right now. For the full broker view of Nashville Airbnb investment property start at the hub; this post is the pre-festival operator and investor read.

What is the booking calendar telling me about CMA Fest 2026?

Across the STR portfolio I have visibility into, the forward booking pattern for the CMA Fest window is consistent with prior years in three ways and divergent in one important way.

Three-night and four-night booking windows are filling first. Properties accepting Thursday through Sunday stays are booked deeper into June than properties with two-night minimums. That has been the pattern every CMA Fest cycle for the last several years; the festival visitor profile is not a one-night traveler.

Premium-priced inventory inside the half-mile core of Broadway and the SoBro corridor is at near-full occupancy for the festival window. The marginal booking the second week of festival run-up has been larger floor plans (3-bedroom and up) and standalone properties with outdoor space. For the buildings I track most closely, the best Nashville buildings for Airbnb pillar lists the high-volume NOOSTR developments where festival-weekend occupancy historically clears 95 percent.

Mid-tier properties two to four miles from the festival core are pricing more conservatively than they did 12 months ago. Operators in East Nashville, Germantown, the Nations, and parts of Inglewood are testing rates 8 to 15 percent below the comparable 2025 festival weekend rates. Some of that is rational supply-response (more permitted properties competing for the same demand pool); some of it is festival-attendance softening that operators are reading into their forward calendars.

The divergent pattern this year: the resale market for STR-eligible product is sending a much clearer signal than the booking calendar. The booking calendar tells you what next weekend looks like. The resale data tells you what the next 24 months of operator economics look like.

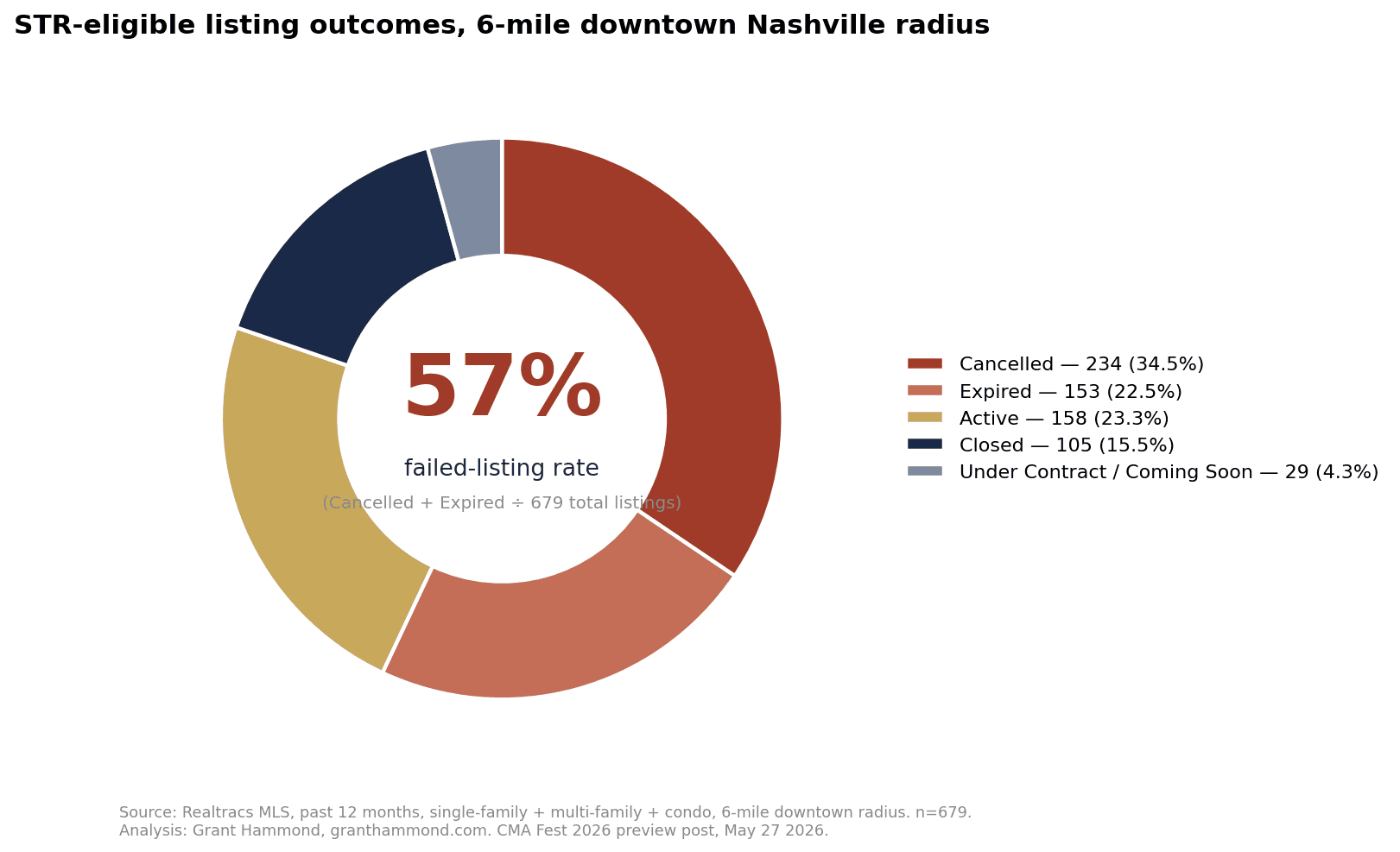

Why is the 57 percent failed-listing rate the real CMA Fest 2026 story?

I pulled every listing on Realtracs flagged as STR-eligible within a 6-mile radius of downtown Nashville for the past 12 months. The sample is 679 properties. The headline number is the one that matters most for anyone underwriting a Nashville STR acquisition in 2026:

57 percent of those listings did not close. 234 were Cancelled by the seller. 153 expired without a sale. 158 are still Active on the market. Only 105 closed, a 15.5 percent close rate against the full universe, or 21.3 percent against just settled outcomes (Closed plus Cancelled plus Expired).

A 57 percent failed-listing rate inside the most demand-rich submarket in Nashville is not a normal market. For comparison, the broader Davidson County resale market over the same window runs closer to a 70 percent close-against-listed ratio across all property types. The STR-eligible subset is failing to close at more than triple the failure rate of the broader market.

What it tells you about underwriting. Listed prices on STR-eligible product are above what buyers will close at. The asking-price ceiling that operators set against 2022 to 2024 festival-revenue assumptions is wider than the current bid-price ceiling that today’s investors are willing to underwrite. When 57 percent of listings fail to close, the bid-ask gap inside the submarket is structurally wide, and seller flexibility is going to open up materially the further you get from peak festival weekends.

What it tells you about the next 6 months. If you are evaluating Nashville STR acquisitions, the post-CMA Fest window (mid-June through early August) is the period when seller flexibility on under-performing listings will be highest. Sellers who listed against an optimistic spring assumption and watched their listing sit through the festival peak are sellers with a real reason to negotiate by mid-July.

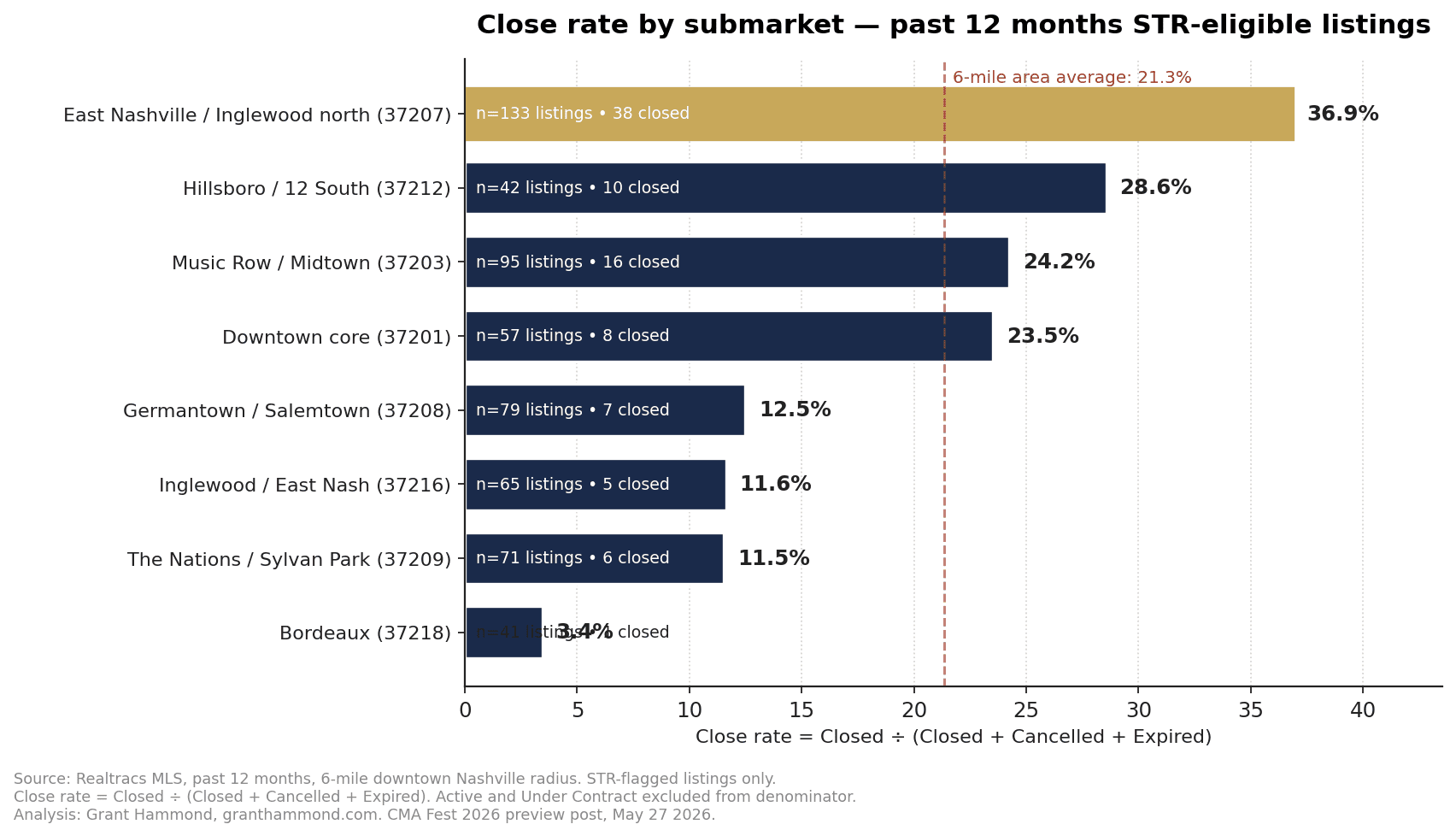

How do submarket close rates vary inside the 6-mile downtown radius?

The headline 57 percent failed-listing rate is a sitewide average. The submarket breakdown is where the actual investment thesis lives.

Some highlights from the same 679-listing pull:

East Nashville / Inglewood north (37207). Highest volume by a wide margin, 133 listings, 38 closed. Settled-outcome close rate 36.9 percent, well above the 6-mile average. Median sale price for the closed segment is in the upper $1M band; the new construction supply concentration in this zip is meaningfully different from the rest of the 6-mile area.

Hillsboro / 12 South (37212). 42 listings, 10 closed. Settled-outcome close rate 28.6 percent. Smaller absolute volume but a clear second-tier close rate among the high-velocity submarkets.

Music Row / Midtown (37203). 95 listings, 16 closed. Settled-outcome close rate 24.2 percent. Median sale price for the closed segment is in the mid-$600K range. The submarket is high-volume but close rates are at the sitewide average, not above it.

Downtown core (37201). 57 listings, 8 closed. Settled-outcome close rate 23.5 percent. Tight footprint, predominantly condo inventory.

Germantown / Salemtown (37208) and The Nations / Sylvan Park (37209). Both at 11.5 to 12.5 percent settled-outcome close rate. These are the submarkets where supply has expanded faster than absorption over the past 18 months and where the asking-price-to-bid-price gap is structurally widest right now.

Inglewood / East Nash (37216). 65 listings, 5 closed. Settled-outcome close rate 11.6 percent. The 35 cancellations in this zip are the largest single concentration of cancelled listings in the 6-mile radius and tell you the asking-price ceiling here has moved further from the bid ceiling than anywhere else in the East Nashville footprint.

The actionable read: the gap between the highest-close-rate submarket (37207 at 36.9 percent) and the lowest (37218 at 3.4 percent) is more than 10x. Submarket selection inside the 6-mile downtown radius matters more for STR investment economics in 2026 than the building or floor plan you select inside a submarket.

Which permit and zoning items should every CMA Fest investor re-verify this week?

Before the festival weekend, three permit-and-zoning items should be verified on any property you operate or are evaluating.

Permit type matches operating intent. An OOSTR (Owner-Occupied Short-Term Rental) permit and a NOOSTR (Non-Owner-Occupied Short-Term Rental) permit operate under different rules. The OOSTR framework requires the operator to maintain the property as a primary residence and limits the structure to one short-term rental unit. The NOOSTR framework is the investor-grade permit that does not require operator residency but is restricted by zoning category to specific commercial and mixed-use parcels and to grandfathered residential properties. A property marketed as an investor-grade vacation rental but permitted under OOSTR is a compliance problem; a property where the owner lives part-time but markets to four-night festival visitors needs the OOSTR framework, not the NOOSTR framework. The BL2019-1633 short-term rental in RM zoning guide walks through the framework on the most-frequently-misunderstood zoning category.

Zoning category supports the permit type. The compatibility matrix between Metro Nashville zoning categories and STR permit types is not intuitive. R6, RS5, R8, RM2, MUL-A, and ORI all have different rules; the assumption that “any single-family zone allows any STR” is wrong and the consequence of operating outside permit-zoning compatibility during a high-visibility festival weekend is material.

Operating-permit-good-standing status is current. Metro renewal cycles run on a per-property basis. An expired or in-arrears permit operating during festival weekend draws faster enforcement attention than a quiet residential month would. Re-verify standing this week, not the morning of arrival.

What signals am I watching the week of May 28 through June 3?

Five signals worth tracking in real time the week leading into the festival.

First, forward booking pace for the post-festival week (June 8 to 14). If the post-festival shoulder week books at 70 percent or higher of festival weekend nightly rates, the broader summer 2026 STR demand picture is healthier than the pre-festival rate compression suggested. If it books at 50 to 60 percent, summer revenue projections need to come down.

Second, cancellation activity inside the festival window. A clean festival weekend shows roughly 1 to 3 percent cancellation rate inside the final ten days. Higher cancellation activity (5 percent and up) is usually a leading indicator of festival-attendance softening or of operators raising last-minute rates and losing penny-conscious bookings.

Third, length-of-stay extension requests. Festival visitors who extend Sunday into Monday or Tuesday are typically the segment most likely to return as a Nashville buyer. STR operators positioning for buyer conversion (your guest today as your closing client in 18 months) should track extensions as a lead-quality signal, not just a revenue add.

Fourth, the Nashville Airbnb Market Report baselines for the East Nashville, Germantown, and SoBro submarkets against the festival weekend actuals. The variance between baseline and actuals is the cleanest comparable read on submarket strength.

Fifth, regulatory enforcement chatter. Metro typically increases enforcement visibility during high-profile festival weekends. Investors in non-conforming properties should expect noise-complaint response times to be faster than a quiet residential weekend.

What does this mean if you are buying an STR-eligible Nashville property in the next 90 days?

If you are evaluating a Nashville STR acquisition right now, three things matter more than they did 18 months ago.

The forward-revenue assumption you carry into underwriting needs to reflect the resale signal, not just the booking calendar. When 57 percent of STR-eligible listings within 6 miles of downtown fail to close, the asking-price ceiling sellers are anchoring on is wider than the bid ceiling buyers will hit. If your pro forma assumes a clearing price at the asking-price ceiling, the pro forma is probably 8 to 15 percent optimistic versus where the actual close will land. The Nashville Airbnb revenue and ROI guide walks through the underwriting math operators are running against today’s resale signal.

Permit-and-zoning due diligence is more rigorous than it was 18 months ago. Metro’s enforcement posture has tightened, the buyer pool for properties with documented permit-zoning compatibility is broader than for properties with murky status, and the resale exit math is friendlier when the permit case is clean.

Submarket selection matters more than building selection within submarket. East Nashville, Germantown, SoBro, and the Nations each have different operating economics and very different close rates in the 6-mile resale data above. The property-level differences inside a submarket are smaller than the cross-submarket differences. If you are evaluating two properties in different submarkets at the same price, the submarket question is the question.

FAQ

Is Nashville Airbnb investment still profitable for new entrants in 2026?

Profitable for the right property under the right permit-and-zoning conditions with realistic forward-revenue assumptions, yes. Not as broadly profitable as it was in 2022 to 2024 when supply was thinner. The properties that hold revenue through demand shifts share a profile: NOOSTR (Non-Owner-Occupied) permit, compatible zoning, two-bedroom or three-bedroom footprint, walking proximity to a commercial corridor.

How much does a short-term rental permit cost in Nashville?

Permit fees and renewal cycles change periodically; the Metro Codes Department site is the canonical source for current fees. The cost of the permit itself is a small fraction of the cost of operating a non-conforming property if Metro initiates enforcement; budget the diligence cost, not just the permit fee.

What is the difference between OOSTR and NOOSTR permits in Nashville?

OOSTR (Owner-Occupied Short-Term Rental) and NOOSTR (Non-Owner-Occupied Short-Term Rental) are the two operating frameworks under BL2019-1633, the legislation that replaced the older Type 1, Type 2, and Type 3 permit categories nearly a decade ago. OOSTR requires the operator to maintain the property as a primary residence and limits the structure to a single short-term rental unit; NOOSTR does not require operator residency but is restricted by zoning category to specific commercial, mixed-use, and grandfathered residential parcels. Most investor-grade Nashville STR product operates under the NOOSTR framework; OOSTR is the right framework for owner-occupants who want to short-term rent a guest house, ADU, or a portion of their primary residence.

Should I buy an STR property before or after CMA Fest 2026?

The post-CMA Fest period (mid-June through early July) is historically a window when seller flexibility opens up because the festival booking premium is realized and underperforming operators recognize the year is not going to bail out a marginal acquisition. With 57 percent of STR-eligible listings within 6 miles of downtown failing to close over the past 12 months, seller flexibility on stale listings should be more pronounced this summer than the prior two years. If you have timing flexibility, mid-June through the Fourth of July is a window worth watching. For sellers thinking about exiting, the Sell My Nashville Airbnb broker process covers the listing strategy on the other side of the table.

Related reading. See my Sunday brief on Nashville’s apartment concession wave and what it signals for short-term rental operators.

Sources, methodology, and disclosure

The 57 percent failed-listing rate and the close-rate-by-submarket data above are from a Realtracs MLS pull of every STR-eligible listing within a 6-mile radius of downtown Nashville for the trailing 12 months. Sample size: 679 properties. Close rate is calculated against settled outcomes (Closed plus Cancelled plus Expired); Active and Under Contract listings are excluded from the denominator because their outcomes are not yet determined. Submarkets are grouped by zip code primary assignment.

Booking patterns, revenue compression observations, and submarket reads outside the MLS-derived numbers are based on the broker observation set across active Nashville STR portfolios and 550+ closed short-term rental transactions across Davidson County. Specific revenue ranges are intentionally directional rather than dollar-specific because submarket, building, permit type, and operating quality variance is too wide for a single dollar-figure benchmark to be honest.

Verified broker authority used: 550+ STR transactions, 25 years of Middle Tennessee brokerage, $1 billion+ in career closings.

Broker fees are not set by law and are fully negotiable. All commission and buyer-agency details should be discussed before contract.

This post is informational and is not legal, tax, or compliance advice; permit and zoning verification should be confirmed with Metro Nashville Codes before acquisition or marketing decisions.